35 min read

Accounts Payable Policies: Structure, Template, and Best Practices

Accounts payable policies structure invoice processing organization-wide. Explore their key components, best practices, and automation options.

Accounts payable touches nearly every part of operations. Every invoice must be reviewed, approved, recorded, and paid on time. However, this process quickly becomes inconsistent without clear rules.

Invoices get routed through informal channels, approvals depend on individual judgment, and vendors receive mixed signals about payment expectations. Over time, these small inefficiencies add up to delayed payments, strained supplier relationships, and limited financial visibility.

That’s where accounts payable policies come in. It defines responsibilities, sets approval thresholds, and ensures every payment follows consistent financial controls.

In this guide, we’ll explain what an AP policy should include, how to implement it effectively, and how organizations can keep it aligned with their financial controls and operational needs.

What are accounts payable policies, and why do you need them?

What should be included in your accounts payable policy template?

How can you create an effective accounts payable policy from scratch?

What are the best practices for accounts payable management?

How do you handle special situations in your AP policy?

How can technology improve your accounts payable policies?

How should you communicate and implement your AP policies?

How often should accounts payable policies be reviewed and updated?

How do you monitor compliance and measure AP policy effectiveness?

How do accounts payable policies support risk management and compliance?

Frequently asked questions about accounts payable policies

What are accounts payable policies, and why do you need them?

Accounts payable policies create a clear foundation for how vendor payments and related processes are handled. An AP policy is a structured document that defines a standard approach to invoice management, approvals, and payments.

When applied consistently, these policies improve cash flow control, strengthen the accuracy of accounting records, and reduce costly errors. Organized invoice processing also helps protect against fraud and builds stronger supplier relationships by ensuring payments are handled reliably and on time.

What exactly is an accounts payable policy?

An accounts payable policy is a formal document that defines procedures for invoice processing and vendor payments. Without clear, organization-wide guidelines for how invoices are received, approved, and paid, it becomes difficult to maintain consistent cash flow and financial control.

The accounts payable policy includes several critical components:

- Payment authorization levels — dollar amounts that dictate who is authorized to approve certain invoices.

- Invoice processing workflows — these outline the entire flow from invoice receipt to payment.

- Vendor management protocols — rules for verifying and establishing new vendors and suppliers.

- Payment terms and schedules — normal payment terms to maintain smooth cash flow.

- Internal controls — measures to avoid duplicate, fraudulent, or incorrect payments.

An accounts payable policy supports both compliance and training. For new hires, it serves as a clear guide that explains exactly how to handle specific tasks, reducing uncertainty. Meanwhile, auditors can use it as evidence that proper controls are in place, and managers rely on it to ensure that payment transactions are processed consistently across the organization.

Why are standardized AP policies critical for your business?

Clear standards in an accounts payable policy ensure consistent operations and significantly reduce confusion and processing errors. Without a defined process, team members handle invoices differently, which may lead to late payments, strained vendor relationships, and missed early payment discounts. With a standardized policy in place, every invoice follows the same steps, from verification to approval.

The main benefit of formal AP policies is stronger financial control. With clear policies in place, an organization gains better visibility into spending, can identify unauthorized transactions, and make more accurate cash flow forecasts. Defined approval levels reduce maverick spending and ensure each payment receives the right level of review. Over time, standardized processes also help lower processing costs.

Formal AP policies also improve audit readiness. Internal and external auditors can quickly assess whether proper controls exist and are being followed. Supporting documentation for each transaction creates a clear audit trail, reducing compliance risks and speeding up the audit process. This is especially important for publicly traded companies that must regularly demonstrate effective AP internal controls.

What are the risks of operating without formal AP policies?

If an organization doesn’t have a formal accounts payable policy, it opens itself to various financial and operational risks.

When invoice approval procedures are vague or inconsistent, the fraud risk becomes much higher. An employee might approve payments beyond their authority, duplicate invoices may go unnoticed, or even a fake vendor could be added without proper verification.

Poorly defined processes also lead to more payment errors. Invoices may be paid twice, early payment discounts can be missed due to delays, and vendors may receive incorrect amounts. These mistakes damage supplier relationships and consume the AP team’s time that could be spent on more strategic work.

Compliance failures are another major risk. Without proper documentation and consistent processes, it becomes difficult to demonstrate effective internal controls to auditors. As a result, companies face regulatory fines and raise concerns about the reliability of financial statements. Inconsistent practices also create employee confusion, spread inefficiencies across departments, and increase training time for new hires.

Cash flow management also suffers without standardized payment schedules and approval procedures. When payments aren’t handled in a structured way, companies lack visibility into upcoming cash needs, struggle to maintain healthy working capital, and may fail to negotiate or meet preferred supplier payment terms.

How do AP policies differ across company sizes and industries?

The scope and complexity of accounts payable policies vary depending on the organization’s size and industry.

Smaller companies (typically those with 50 employees or fewer) often rely on simple procedures. Approval authority is usually limited to the owner or financial manager, and the process is more flexible. Still, even basic procedures should be documented to support future growth.

Mid-sized and enterprise organizations require more structured and detailed policies. With multiple departments, locations, and approval workflows, they need multi-level authorizations, clear segregation of duties, and often workflow automation. Their policies must also address more complex scenarios, such as intercompany transactions, PO matching, and department-specific budgets.

Industry-specific considerations also shape policy requirements:

- Healthcare organizations have rigorous requirements concerning vendor credentialing and payment-supporting documentation.

- Government contractors must adhere to the Federal Acquisition Regulation (FAR) with specific approval procedures.

- Manufacturing companies implement AP policies as part of their supply chain system and inventory controls.

- Financial services firms have increased safeguards concerning fraud and require extensive audit trails.

Organizations in highly regulated industries typically require stricter, well-documented controls. In contrast, technology companies often prioritize speed and automation over detailed manual procedures.

The key is to align your accounts payable policy with your company’s size, operations, and regulatory responsibilities to apply the right level of control without adding unnecessary complexity.

What should be included in your accounts payable policy template?

A complete accounts payable policy template outlines clear guidelines for all payment-related activities within a business. When developing the template, it’s important to balance thoroughness with clarity: it should cover all relevant payment scenarios while remaining easy to understand and follow. A well-designed template also makes implementation smoother and more consistent across the organization.

What are the essential components every AP policy must have?

It’s important to identify key elements that should be present in all AP policies to guarantee that appropriate business rules and financial controls are in place. Without the following features, key elements of the process won’t be implemented:

- The scope and purpose statement defines the extent to which this policy applies and to what activities it applies to.

- Roles and responsibilities define the tasks of the AP staff, approvers, and management.

- Invoice receipt and verification procedures describe the processes by which invoices are received, entered, and verified.

- Approval workflow and authorization matrix define who has the authority to approve payments at different levels.

- Payment processing schedules describe the times and the method of payments to be made.

- Vendor management procedures deal with the processes to set up, manage, and terminate relations with suppliers.

- Exception handling procedures address disputes, rush payments, and special circumstances.

- Internal control procedures and segregation of duties establish preventive controls to reduce the risk of fraud and unauthorized payments.

- Record retention requirements describe how long the relevant documents are supposed to be kept.

- Policy review and update procedures describe when the policy is supposed to be updated.

The policy should also reference related documents, such as the expense reimbursement policy, procurement policy, corporate credit card policy, and any other guidelines connected to the accounts payable process.

How should you structure your invoice approval workflow?

The invoice approval workflow is the most critical operational element of an accounts payable policy. It should provide strong controls without creating delays in the payment process.

The workflow begins when an invoice is received by mail, email, or through an electronic invoicing system. The AP team first reviews the invoice to confirm that all required information is included:

- Vendor information

- Invoice number and date

- Itemized charges

- Payment terms

Invoices that don’t include the required information are returned to the vendor for correction.

Most organizations use three-way matching to validate invoices. This process compares the invoice with the original purchase order and the receiving document to confirm that the goods or services were both ordered and received. If any discrepancies are found, they must be investigated and resolved before payment is approved.

The approval path depends on the approval matrix defined in the AP policy. Factors such as invoice amount, department, and account code (or a combination of these) determine who must review and approve the invoice. The policy should also set clear timeframes for approvals. Typically, each approval step is expected to take two to three business days.

Many organizations use automated workflow systems to route invoices electronically and send reminders for pending approvals. Compared to manual or paper-based routing, automation significantly reduces processing time and delays.

What payment terms and conditions should you define?

Clearly defined payment terms help prevent misunderstandings with suppliers and support consistent cash management. An accounts payable policy should allow the organization to apply standard terms while allowing approved exceptions that benefit the company.

The policy should also explain how payment terms are negotiated and approved. Standard terms are applied automatically, while any exceptions must be formally documented and approved by finance management. Establishing preferred payment terms helps the organization align with its cash conversion cycle and manage working capital effectively.

The policy should clearly outline procedures for late payment penalties and early payment discounts. It should specify whether the company will take advantage of available discounts, who has the authority to approve them, and how any penalties for late payments to vendors are handled.

Which vendor management guidelines need to be documented?

Vendor management guidelines ensure supplier files are kept up to date and that all vendors meet organizational requirements. The procedures should help avoid fraudulent activity and improve payment process efficiency.

In terms of vendor onboarding, a plethora of documentation needs to be collected prior to any payment. New vendors need to fill out a standard vendor information form, providing details such as legal business name, tax ID, payment address, and banking information for electronic payments.

The AP team will then check the information using third-party databases or verify banking information directly with financial institutions. In some cases, additional background checks may be required for security purposes.

A best practice is to collect Form W-9 from domestic vendors to ensure accurate 1099 reporting at the end of the year. For foreign vendors, the required forms depend on the country’s tax treaties and payment methods. Failing to collect proper tax documentation can create compliance risks and lead to penalties during audits.

Procedures for maintaining the vendor master file ensure that vendor information stays accurate and prevent duplicate entries in the system. The policy should clearly specify which employees are authorized to add, update, or deactivate vendor records. To reduce risk, employees who enter or modify vendor data shouldn’t be the same ones who approve payments.

Vendor files should be reviewed regularly to identify inactive vendors, merge duplicates, and verify contact details. Typically, each active vendor receives an annual verification request to keep information current and detect any unauthorized changes to payment data.

How do you establish clear authorization limits and segregation of duties?

Authorization limits and segregation of duties form the foundation for internal AP controls. These procedures limit the ability to spend unauthorized amounts of money and minimize the risk of fraud by ensuring no single person can execute a process from initiation to payment.

Here’s a common authorization matrix structure example:

The authority matrix can be adjusted based on company size and risk tolerance. Small companies often rely on top executives for approvals, while larger organizations typically use multi-level approval systems. Industries with regulatory requirements may also include mandated authorization levels.

Segregation of duties ensures that different employees handle separate steps in a process. For example, the person who orders goods shouldn’t also approve the invoice for payment, and the employee authorizing the payment shouldn’t process it or reconcile bank accounts. These divisions create checks and balances that make fraud easier to detect.

In small companies with limited staff, it may not be possible to fully separate duties. In such cases, the AP policy can include compensating controls, such as requiring owners to verify all payments, mandating vacation days, or conducting periodic surprise audits, to maintain proper oversight.

How can you create an effective accounts payable policy from scratch?

Creating a new accounts payable policy from scratch requires significant research and input from stakeholders. A poorly designed policy can either be too strict to follow or too vague to be useful. Therefore, policy development should aim for a balance between detailed guidance and practical, achievable standards.

Where should you start when developing your AP policy?

When developing an AP policy, review the current payment system to pinpoint the primary issues. Map out the path each invoice takes, pinpoint weaknesses, and assess how existing controls function. This analysis will highlight the areas the new policy needs to address.

Another aspect to consider is the range of industry standards and regulatory rules that are specific to your field. A manufacturing company must follow compliance rules that a healthcare provider or government contractor doesn’t, and vice versa. The policy framework should establish mandatory controls and incorporate proven best practices to improve effectiveness.

Finally, review existing financial policies to ensure alignment. The accounts payable policy should be consistent with procurement, reimbursement, and budget authorization policies. Identify overlaps and make sure all financial processes work together smoothly.

Who should be involved in the policy creation process?

Policy development requires the participation of multiple departments to ensure that the final document addresses real operational needs:

- AP staff offers the front-line perspective on the everyday processing challenges and workflow constraints.

- Finance leadership defines control requirements and ensures alignment with financial reporting needs.

- The procurement team ensures that the purchase order process flows smoothly into the invoice approval process.

- Department managers verify that the approval hierarchies correspond to the organizational structure and budget authority.

- The IT department confirms the technical feasibility of system integrations and automation measures.

- Internal audit makes sure that control objectives will satisfy compliance and risk management needs.

The CFO or another finance controller should sponsor the policy to ensure it has sufficient resources and executive support. The actual drafting should be done by AP managers, who handle the day-to-day processes and can create practical, actionable procedures rather than theoretical guidelines.

What questions should you ask to identify your company's specific needs?

Well-structured discovery questions help define policy requirements based on organizational traits and operational realities. You can start with an assessment of volume and complexity:

- How many invoices does the company process monthly?

- What percentage requires purchase order matching versus non-PO processing?

- How many vendors are active in the system?

Try to examine current pain points directly with the following questions:

- Where do invoices get stuck in the approval process?

- Which vendor relationships have been damaged by payment delays?

- What fraud or error incidents have occurred in the past two years?

Evaluate the organization’s current resource limitations and technological capabilities:

- Does the organization have AP automation software or rely on manual processes?

- How many staff members handle accounts payable functions?

- What approval turnaround times are realistic, given current workloads?

The policy should be realistic, reflecting the organization’s current resources rather than assuming unlimited capacity. At the same time, it should account for future growth and scalability by asking questions such as:

- Will the company expand into new markets or acquire other businesses?

- Does the vendor base change seasonally?

Policies that are designed only for present-day operations tend to become outdated relatively quickly as businesses grow and evolve.

How do you align AP policies with overall financial controls?

AP policies are part of a broader internal control framework and can’t work in isolation. For organizations subject to Sarbanes-Oxley (SOX) requirements, AP policies must support specific SOX compliance objectives.

AP should also be closely integrated with spend management systems. The policy must define how fund availability is verified before invoices are approved for payment. If a purchase exceeds its budget, the policy should establish clear escalation procedures. These measures ensure that unauthorized spending is prevented while allowing essential business expenditures to be approved quickly when needed.

The ERP system must be configured to enforce the requirements of the AP policy through system controls. For example, if the policy includes an authorization hierarchy, it should be implemented in the system’s workflow rules. The policy should also clearly specify which controls are automated by the system and which rely on user compliance, as automated controls provide greater assurance.

Routine reconciliations connect AP with cash management and the general ledger. The policy should define how often these reconciliations occur, who is responsible, and how discrepancies are addressed to ensure AP records remain accurate.

What common mistakes should you avoid during policy development?

Excessive complexity is the number one policy killer. Companies may produce one-hundred-page, step-by-step instructions on what to do in every conceivable situation, yet an employee will almost certainly be unable to follow them during daily work. A well-designed policy focuses on detailed standard procedures while clearly documenting exceptions for unusual situations.

The policies formulated without user input result in documents that read well in theory, yet don't work in practice. AP staff can identify controls that are practical and won’t create workflow inefficiencies. Without their input, policies are often ignored or altered as soon as they are implemented.

If a policy doesn’t take existing systems into account, it can create requirements that the current software can’t handle. For example, asking for three-way matching when the ERP system can’t do it automatically forces staff to do manual workarounds, which slow down processing and increase mistakes. Policies should match what the system can do, or there should be a plan to upgrade the system to support them.

Inaccurate or unclear wording can cause confusion and lead to inconsistent application of policies. Phrases such as “quick approval” or “adequate documentation” mean various things for different people.

Specifying exact timeframes and listing the required documents for approvals helps remove this ambiguity. Undefined terms such as “urgent payment” are especially risky, as they leave room for misuse and differing interpretations of what qualifies as “urgent.”

What are the best practices for accounts payable management?

Best practices for accounts payable management bridge the gap between theoretical policies and actual operations. They accelerate invoice processing times, minimize inaccuracies, and provide greater internal controls over their operations.

It’s important to remember that best practices are relevant for organizations of all sizes, but the complexity of their implementation may vary based on factors like transaction volume and technological capabilities.

How can you implement a robust three-way matching system?

In a three-way matching system, the purchase order, receiving document, and invoice are compared to ensure that payments are only made for approved purchases and received goods. This process helps prevent paying for items that were not ordered, not received, or overcharged.

Most modern AP systems perform invoice reconciliations automatically using the following documents:

- The purchase order establishes what was ordered and at what price.

- The receiving report confirms physical receipt and quantity.

- The vendor invoice requests payment.

Discrepancies in quantity, price, or terms trigger predetermined exception workflows that demand manual investigation before payment can proceed.

Tolerance thresholds define when discrepancies between documents will hold a payment versus when they can be approved automatically. For example, a $5 difference on a $10,000 invoice is minor, but the same $5 on a $100 invoice is significant. Most organizations use percentage-based thresholds, such as “5% quantity deviation, 2% price deviation.”

Three-way matching can be done manually for a small number of invoices, but it becomes impractical beyond about 100 invoices per month. Automating the process with an ERP or AP system can reduce the matching cycle from days to minutes and ensure consistent application of the policy.

What are the most effective invoice processing procedures?

A key part of an efficient AP process is invoice receipt centralization. A centralized AP inbox (either physical or electronic) guarantees that all incoming invoices are received and recorded immediately. A decentralized receiving system commonly results in missed invoices, duplicate payments, and loss of early payment discounts.

Invoice validation should happen within 24 hours of receipt. AP staff are responsible for verifying that invoices contain the essential information, including:

- Vendor name

- Invoice number

- Date

- Line items

- Payment terms

Incomplete invoices are returned immediately instead of waiting for information to be confirmed or modified.

Accurate coding is essential to ensure expenses are charged to the correct account and budget. Invoices should be coded by the department responsible for the budget, rather than by AP staff who may not know the context of the purchase. AP staff should still review the coding to catch any obvious errors before the invoice moves to the next approval stage.

Digital workflows prevent delays caused by handling physical paper. Invoices are scanned upon receipt using Optical Character Recognition (OCR) technology and routed electronically to approvers based on business rules. System reminders flag overdue approvals, and real-time dashboards show the status and location of every invoice in the workflow.

How should you handle exceptions and discrepancies?

Exception handling procedures prevent delays when an invoice doesn’t match the related documents or when a dispute arises. Clear procedures define how and when exceptions are addressed, ensuring they don’t remain unresolved for long periods.

For price discrepancies, the purchasing department should be contacted to determine whether the price changed after the PO was issued or if the vendor billed incorrectly. AP supervisors can approve minor discrepancies within a set threshold, while larger issues require the buyer to investigate and potentially negotiate with the vendor.

Quantity discrepancies between the invoice and the receiving report may be caused by receiving or billing errors. The warehouse or the receiving department has to verify whether the product was actually delivered. Partial shipments are common and may require prorated payments or partial invoice approval instead of rejection.

For disputed invoices, the process should be clearly documented with defined resolution timeframes. Vendors must be notified within five business days when an invoice is placed on hold, including the reason for the dispute and the expected resolution timeframe. Weekly tracking of open disputes ensures that no issues are overlooked and helps maintain strong vendor relationships.

The policy should establish escalation procedures for disputes that cannot be resolved at the AP level. Any dispute older than 30 days should be escalated to finance leadership. This approach prevents issues from remaining unresolved indefinitely, protecting vendor trust.

What internal controls prevent fraud and errors in AP?

Accounts payable internal controls create multiple checkpoints to detect errors and prevent fraud. The most effective controls are automated, enforced by the system, and independent of manual actions.

A key principle in fraud prevention is segregation of duties. For example, an employee who enters vendor details into the system shouldn’t also have the authority to approve payments to that vendor. These measures ensure that at least two people would need to collude to commit fraud, significantly reducing the likelihood of it occurring.

Controls over the vendor master file help prevent fraudulent vendor schemes. Adding a new vendor should always be supported by proper documentation, such as W‑9 forms and business verification. Changes to a vendor’s bank information should be verified by calling a known telephone number, not the number provided in the change request, to prevent unauthorized payment redirection.

Before processing payments, the system should automatically check pending invoices against existing records for potential duplicates by comparing vendor, amount, and date. Differences in invoice numbers or slight variations in dates may indicate errors or possible fraud and should be reviewed before payment.

Ongoing vendor statement reconciliation reveals misapplied payments or unauthorized invoices that may have slipped through the approval process. Monthly reconciliation of high-volume vendors would catch these transactions before they start compounding on top of each other.

How can you optimize your payment schedules and take advantage of early payment discounts?

Strategic payment timing is the trade-off between cash flow preservation and cost-saving opportunities. Random vendor payments often miss opportunities for discounts and can harm vendor relationships due to unpredictable schedules.

Scheduling batch payments on fixed days each week improves predictability for suppliers and efficiency for AP staff. Many companies, for example, run a weekly payment batch on Wednesday or a bi-weekly batch timed to maintain steady cash flow. This approach makes accounts payable forecasting easier and helps ensure no invoices are overlooked.

Early payment discounts, such as 2/10 Net 30, offer substantial annualized returns, equivalent to approximately 36% annual interest. The accounts payable policy should mandate taking these discounts whenever the company has enough cash for them. Few alternatives offer comparable risk-free returns.

Payment method optimization reduces costs while accelerating processing speed. For example, ACH payments cost significantly less than checks, typically $0.50 versus $3–$5 per payment with printing, mailing, and reconciliation costs. Virtual credit cards can generate rebates while extending days payable outstanding (DPO).

The policy should define acceptable payment methods and set guidelines for any exceptions, allowing the company to optimize its payment processes.

Vendor negotiations can provide benefits beyond standard market terms. Leading vendors often offer better payment terms or larger early payment discounts to preferred clients. AP departments should work closely with procurement to identify these opportunities during contract renewals.

How do you handle special situations in your AP policy?

Without clear procedures for handling non-standard cases, decisions can become inconsistent, leading to confusion and frustration among stakeholders. Special situations should have documented exception processes that preserve controls while allowing necessary flexibility. The policy should outline clear steps so staff don’t have to create ad hoc solutions each time.

What procedures should govern rush or emergency payments?

An emergency payment is one that bypasses the normal approval timelines due to urgent business needs. The AP policy should clearly define what qualifies as a true emergency to prevent misuse of the expedited payment process.

Legitimate emergencies include:

- Critical equipment repairs (halt production)

- Legal settlements (court-imposed deadlines)

- Utility shutoffs (threaten business operations)

- Situations where payment delays create safety hazards

Regular vendor payments, forgotten invoices, and the results of poor planning shouldn’t qualify as true emergencies.

Expedited approvals require a written justification from the requesting department, the signature of the department head, and, for larger amounts (typically over $5,000), the CFO’s approval. If a same-day wire transfer is requested, treasury management must also authorize it to confirm cash availability. All emergency payments should be fully documented, including a written memo, an explanation, and the steps taken to prevent similar situations in the future.

How should you process employee reimbursements and expense reports?

Reimbursement procedures for employee expenses are typically handled separately from vendor payments. Employees should submit expense reports within 30 days of incurring them, and original itemized receipts are required—credit card statements alone aren’t sufficient.

The expense report approval process follows the same structure as invoice approvals. Employees can’t approve their own expenses; submissions must be approved by their manager or, if necessary, the next-level manager. The policy should also specify per diem rates, IRS travel rates, and limits for meals, hotels, and entertainment.

Prohibited expenses that require explicit listing to avoid confusion include:

- Alcoholic beverages (except business meals with clients)

- Personal travel expenses or family member costs

- Fines, penalties, traffic violations

- Expenses without proper documentation

The reimbursement timing should be consistent: employees should receive reimbursement within 10 days of submitting compliant expense reports. Delayed reimbursements lead to negative employee morale and financial difficulties for individuals.

What policies apply to international vendors and foreign currency payments?

International vendor payments involve additional considerations, such as tax obligations and foreign currency management, which are not present with domestic payments. The AP policy should clearly address currency selection, foreign exchange handling, and tax withholding requirements.

Companies must decide whether to pay in the vendor’s currency or in USD. Paying in the vendor’s currency shifts the foreign exchange risk to the company while removing it for the vendor. The policy should also specify who is authorized to approve currency changes and whether FX hedging is required for larger payments.

Tax documentation becomes extremely important for cross-border payments. Foreign vendors must complete W-8BEN or W-8BEN-E forms to establish tax treaty benefits and withholding rate applicability. Payments to vendors in non-treaty countries may require 30% withholding tax, which must be remitted to the IRS. The policy should assign responsibility for this process to AP staff with international tax knowledge or require them to consult qualified tax advisors.

International payments also incur wire transfer fees, typically charged per transaction. The policy should clearly state how these fees are handled—either absorbed by the company or deducted from the payment amount.

How do you manage recurring payments and subscriptions?

Regular payments and subscriptions should be actively monitored to avoid missed cancellations and unexpected charges. Many items (such as software subscriptions, insurance premiums, lease payments, and service agreements) renew automatically without prior notice.

The policy should require AP to maintain a centralized subscription register, tracking the following details:

- Vendor name

- Service description

- Payment amount

- Billing frequency

- Renewal date

- Contract owner

- Cancellation notice requirements

Extensive visibility prevents duplicate subscriptions for similar services and ensures cancellation when services are no longer needed.

For all subscriptions exceeding $5,000 per year, a renewal approval should be required 60 days prior to the expiration date of the contract. The contract owner is responsible for verifying the need for the particular subscription and ensuring that sufficient budget is available. Contract clauses for automatic renewal should be flagged in the system so that approval workflows are triggered, rather than allowing payments to process automatically.

Recurring credit card charges can be hard to control because they often bypass standard invoice approval procedures. The policy should require prior approval for all recurring charges and ensure that monthly credit card statements are reviewed by someone other than the cardholder.

What are the guidelines for handling disputed invoices?

Invoices with disputes should be formally placed on hold to prevent payment processing. Each disputed invoice should include a reason code and an expected resolution date to ensure visibility and proper tracking.

Disputes tend to fall into several common categories:

- Pricing discrepancies where invoiced amounts exceed purchase order prices

- Quantity issues where billed quantities differ from the receiving documentation

- Quality problems where goods are defective, or services are unsatisfactory

- Invoices for goods never ordered or received

Each type of dispute should be handled according to its category. Clear communication protocols must be established, with vendors notified in writing within five business days and provided with the documentation required to resolve the issue. The policy should specify whether AP staff or the originating department is responsible for vendor communication.

No dispute should remain “pending” indefinitely. Disputes unresolved after 30 days should be escalated to procurement management, and those exceeding 60 days require CFO review to determine whether to approve accelerated payment for settlement or consider ending the vendor relationship. Maintaining dispute logs protects the company in case vendor relationships escalate to litigation.

How can technology improve your accounts payable policies?

Technology turns policies from abstract documents into concrete actions embedded in daily business processes. Automation reduces manual effort while ensuring compliance through proper approvals and real-time transaction monitoring.

According to Ardent Partners, organizations with highly automated AP systems achieve up to 81% faster invoice processing times and nearly 80% lower processing costs.

What automation tools can streamline AP processes?

AP automation software minimizes manual, repetitive tasks that consume staff time and increase the risk of human error. OCR extracts data directly from scanned invoices, removing the need for manual data entry. Automated three-way matching then compares the invoice with the purchase order and receiving report without manual review.

Workflow automation guides invoices to the designated approvers automatically according to set parameters, such as amount, department, and account coding. Reminders are sent to notify individuals of outstanding approvals, and past-due items are escalated automatically. Electronic payments are processed via ACH files or virtual cards directly from approved invoices, removing the need to print and mail checks.

Exception management tools identify duplicate invoices, missing purchase orders, and breaches of the approval policy prior to payment processing. These automated controls ensure consistent application of policies at a scale and level of reliability that manual controls simply can’t match.

How can Precoro help standardize AP workflows?

Precoro offers procurement and AP automation capabilities, enforcing policy compliance via configurable workflows. The platform routes invoices according to your internal approval structures and enforces spending limits and budget constraints. Approval SLAs set a target timeframe for each approver to review and approve an invoice. This feature ensures that invoices move quickly through every step of the approval workflow.

Vendor invoices are received through a centralized AP inbox, where they are automatically captured and processed. Optical Character Recognition (OCR) extracts key invoice data from the document, reducing manual data entry and minimizing errors. Vendor records are stored in a centralized system and can be managed through a secure Supplier Portal that simplifies updates and speeds up communication.

With Precoro's spend management functionality, companies can monitor spending against assigned budgets in real time. Purchases that exceed budget limits are flagged before approval, preventing surprises during month-end reconciliation. Integration with existing ERP systems keeps financial data aligned while preserving the specialized workflow capabilities that standard accounting software may lack.

By combining procurement controls with AP automation, organizations gain an end-to-end solution that enforces policies consistently throughout the entire purchase-to-pay cycle.

How does AP software ensure policy compliance?

AP software helps ensure policies are followed and documents all changes. The system’s built-in approval rules limit what each employee can approve based on their spending authority. Approval steps are required in a set order, so the person who requested a purchase can’t also approve it.

The system also checks that invoices have all required information (like tax ID numbers, purchase order numbers, or other documentation) before they can be processed. This prevents the risky “pay now, provide documents later” approach that often causes compliance problems.

Audit trails track every action on an invoice (who recorded it, when it was approved, and any changes made). These records support internal audits and help verify that controls are working correctly. Automated compliance reports can also flag policy violations, such as splitting purchases to bypass approval limits or paying invoices without proper authorization.

What role does electronic invoicing (e-invoicing) play in modern AP policies?

Electronic invoicing speeds up invoice receipt and prevents the data entry errors common with paper-based processes. Vendors submit invoices directly into the AP system via web portals or EDI interfaces, capturing data in a structured format without relying on OCR from PDFs.

E-invoicing policies should specify accepted invoice formats, submission methods, and vendor onboarding procedures. For vendors unable to submit electronically, a paper alternative should be defined (typically scanned and entered by AP staff).

Regulatory requirements for e-invoicing vary by country. Some regions mandate specific invoice formats, while others allow more flexibility. The policy should reference these regulations and assign responsibility for keeping the policy up to date.

How can you integrate AP systems with your ERP and accounting software?

Seamless integration between AP automation software and the ERP prevents duplicate data entry and keeps all financial information in sync. Invoices approved in the AP system flow automatically into the general ledger, removing the need for manual journal entries or imports.

The integration should be bi-directional. Purchase orders created in the ERP appear in the AP system for invoice matching, and any updates to vendor master records in either system are automatically reflected in the other. Payment information should also be sent back to the ERP, updating cash accounts and vendor balances to ensure accuracy and consistency.

Real-time integration gives immediate financial visibility, unlike batch uploads that cause delays. However, it also demands stronger system reliability and error handling. Define how real-time data transfers are monitored, verified, and reconciled to prevent discrepancies.

What are the benefits of cloud-based AP solutions for policy enforcement?

Cloud-based AP systems provide far greater accessibility than on-premise solutions. Approvers can review and authorize invoices from anywhere, even on their mobile phones, reducing delays caused by travel or remote work. This accessibility allows the payment process to proceed smoothly without compromising approval controls.

Cloud services ensure your system always meets current standards. Automatic updates keep the system compliant with changing tax regulations and payment rules, removing the need for costly and time-consuming manual software upgrades.

Disaster recovery is built in, so invoice data and approval logs remain accessible regardless of office location. Business continuity features allow payment processing to continue during office closures, without the need for redundant systems.

Cloud solutions also scale easily to handle fluctuations in demand. Seasonal businesses or fast-growing companies can add users and processing capacity without purchasing new hardware or undertaking complex implementation projects.

How should you communicate and implement your AP policies?

Effective policy implementation demands clear communication and structured training programs. Organizations that only distribute policy documents without proper rollout planning tend to encounter resistance, confusion, and inconsistent adoption as a result. Successful implementation, on the other hand, treats policy deployment as a change management initiative, not a documentation exercise.

What's the best way to roll out new AP policies to your team?

Policy rollout should begin with advance notice and leadership endorsement. Announce the new policy at least 30 days before it takes effect, and clearly explain why changes are necessary and how they are going to benefit the organization. Visible support from the CFO or controller reinforces that compliance with the policy is mandatory.

A phased implementation is usually more effective than an abrupt rollout, especially for complex policy changes. Start with a pilot group, such as one department or location, to identify and resolve issues before launching company-wide. This approach allows the policy to be refined based on real-world feedback and helps create internal champions who can support the broader rollout.

Communication should clearly explain how the policy affects each role. AP staff need detailed process training, while approvers must understand their responsibilities and authorization limits. Department managers, procurement teams, and executive leadership each require different information. Tailored communication prevents information overload and ensures every group receives relevant, practical guidance.

How do you train employees on policy requirements and procedures?

New training programs should account for varying learning styles and experience levels. Live sessions allow employees to ask questions and discuss ambiguous situations that written policies alone can’t clarify. Recorded sessions are also valuable as they help remote staff and serve as reference material for future hires.

Hands-on practice in the actual AP system is more effective than theory alone. Walk employees through sample transactions covering invoice entry, approval routing, and exception handling. Include common scenarios, such as invoices without purchase orders, pricing discrepancies, or urgent payment requests.

Role-based training ensures each employee focuses on what they actually do. AP clerks need detailed guidance on invoice processing, while approvers only need to understand review and authorization responsibilities. Quick reference guides summarizing key requirements for each role add an extra layer of practical support for employees.

What documentation and resources should be readily accessible?

Employees need easy access to policy documentation without the need to search through file servers or email HR for copies. The full policy document has to be available on the company intranet with clear version dating. Even then, most employees might still prefer quick reference materials over comprehensive policy manuals for daily use.

Flowcharts and checklists help distill complex procedures into simple visual guides. For example, an invoice approval flowchart showing decision points and routing paths would help employees navigate the process correctly. Checklists for common tasks, such as new vendor setup or expense report submission, can dramatically reduce common errors and ensure consistency.

Frequently asked questions (FAQ) can complement formal policy language by addressing common scenarios. Using real examples helps make abstract policy requirements more concrete and easier to understand. The FAQ should be updated regularly based on the questions employees actually ask, rather than only on situations policy writers anticipate.

How can you ensure vendors understand and comply with your policies?

Vendor compliance begins during onboarding when new suppliers are added to the system. A clear set of expectations can prevent a lot of problems before the first invoice arrives. The vendor onboarding package should clearly cover the following:

- Payment terms

- Invoice submission requirements

- Required documentation

- Contact information for AP inquiries

Invoice submission guidelines must be clear and detailed, specifying required formats, essential information, and approved delivery methods. Indicate whether invoices should be emailed to a dedicated AP inbox, submitted through a vendor portal, or sent via EDI. List mandatory details such as purchase order numbers, itemized charges, and tax identification numbers. Vendors can’t comply with requirements that are unclear or undocumented.

If a vendor submits a non-compliant invoice, the rejection notice should clearly explain what is missing or incorrect, rather than sending a generic “policy violation” message. Educating vendors on corrections helps maintain strong relationships, though repeated non-compliance may need to be escalated to procurement for performance discussions.

Regular vendor communications (such as quarterly newsletters) can reinforce policies, announce updates, and recognize suppliers who consistently submit accurate invoices. Proactive communication prevents errors and demonstrates that the organization values its vendor partnerships.

What communication channels work best for policy updates?

Policy changes require multi-channel communication to ensure message delivery. Email announcements reach most employees but often go unread amid regular inbox clutter. Follow up with team meetings, intranet posts, and system login notifications in order to reinforce the message.

System notifications within AP software can serve as timely, point-of-use reminders. Pop-up messages on login or inline alerts during transaction processing provide employees with the right information exactly when they need it. However, too many alerts can cause notification fatigue, so use this channel only for critical updates.

Version control is equally important. Every policy document should clearly show its effective date and version number. Keep an archive of previous versions for audit purposes, while ensuring that only the current version is accessible through standard channels. Confusion about which policy is active can create compliance issues and weaken overall policy authority.

How often should accounts payable policies be reviewed and updated?

Accounts payable policies require regular review to remain effective as business conditions and regulatory requirements evolve. Static policies become outdated quickly, creating gaps between documented procedures and actual business needs.

What triggers a mandatory AP policy review?

Annual reviews should occur on schedule, but there are also specific events that demand immediate policy evaluation regardless of the regular schedule.

Regulatory and compliance triggers:

- Changes to tax laws that affect vendor reporting or withholding requirements

- New SOX controls or audit findings that require enhanced procedures

- Industry-specific regulations that impact payment documentation

Organizational changes:

- Mergers, acquisitions, or divestitures that alter the company structure

- Implementation of new ERP or AP automation systems

- Significant headcount growth that requires updated authorization matrices

Operational triggers:

- Fraud incidents or control failures that reveal policy weaknesses

- Repeated vendor complaints about payment processes

- Process bottlenecks that cause consistent approval delays

High-volume invoice processors or organizations in heavily regulated industries may benefit from semi-annual reviews rather than annual cycles. The review process should involve AP staff, finance leadership, internal audit, and procurement to capture perspectives from all stakeholders affected by policy requirements.

How to manage version control and policy change history

Version control prevents potential confusion about which policy requirements are currently active. Each policy revision should receive a new version number and an effective date that should be displayed prominently on the first page. The document footer should also include the version number, approval date, and next scheduled review date.

Change logs keep policy updates transparent. A summary table at the start or end of the document should list each version, its effective date, modified sections, and a brief description of changes. This record helps employees understand why policies were updated and allows auditors to track control effectiveness. Retired versions should be archived according to retention rules and clearly marked to prevent accidental use.

How do you monitor compliance and measure AP policy effectiveness?

Monitoring and measurement transform accounts payable policies from theoretical documents into extensive frameworks for accountability. Organizations that track performance metrics can identify problems early on and demonstrate continuous improvement to both stakeholders and auditors.

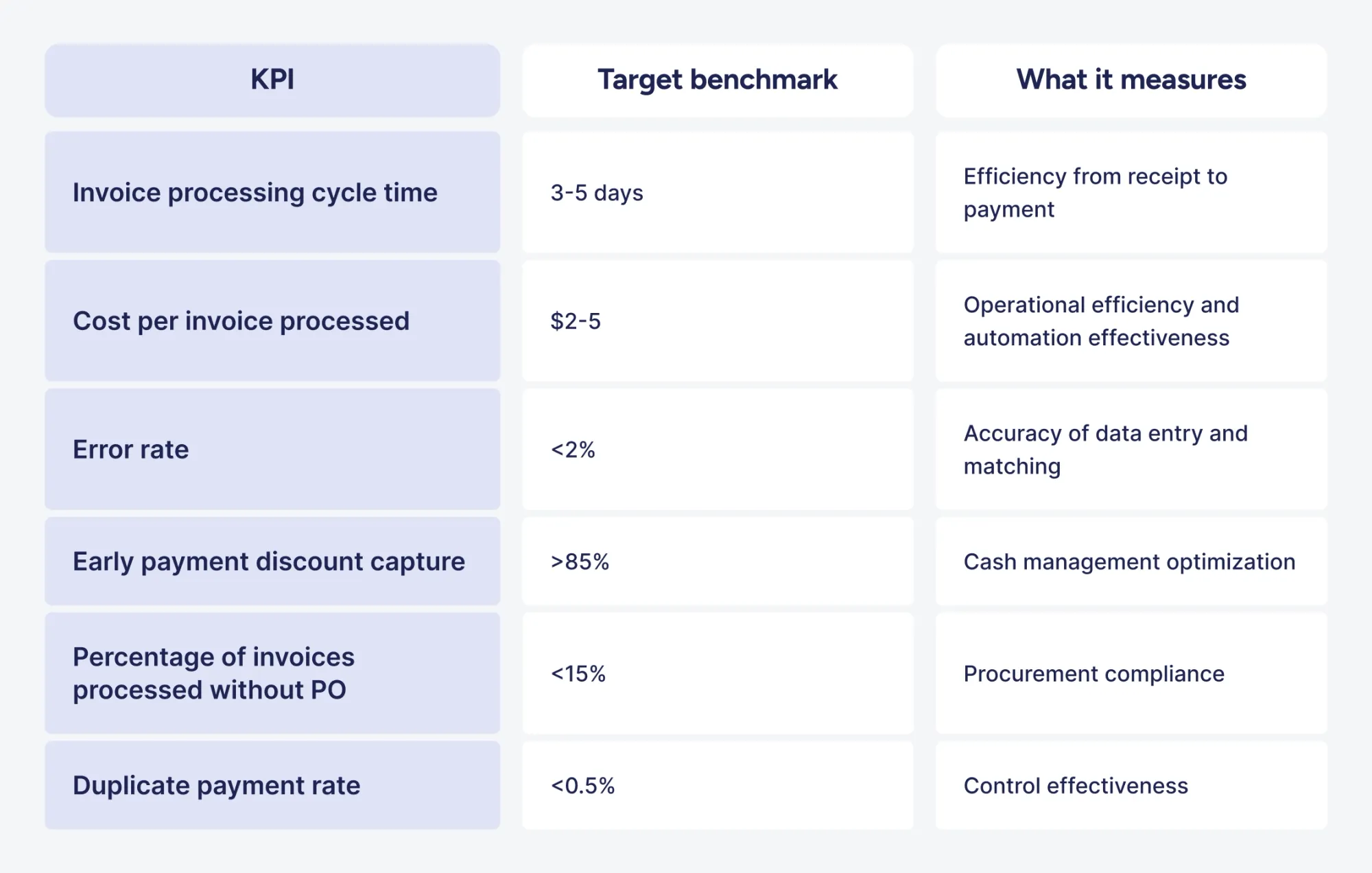

What KPIs should you track to measure AP performance?

Key performance indicators provide objective evidence of whether AP policies are achieving intended results. The most critical metrics include:

Days payable outstanding (DPO) shows how long a company takes to pay its suppliers. While a longer DPO can preserve cash, paying too slowly can harm vendor relationships and forfeit early payment discounts. The ideal DPO balances cash flow with supplier satisfaction.

Touchless processing rate measures the share of invoices processed automatically, without manual intervention. Higher rates indicate strong automation, accurate invoice data, and good compliance with company policies.

How often should you audit your accounts payable processes?

Internal audits should be conducted quarterly for high-risk areas, such as vendor master file changes, employee reimbursements, and payments above authorization limits. These targeted reviews help catch control issues before they become bigger problems.

A full accounts payable audit should be performed annually, covering all policy requirements. It checks whether procedures are followed, verifies segregation of duties, ensures authorization limits are enforced, and reviews how exceptions are handled. Any issues found should lead to immediate corrective actions and policy updates.

External auditors also review AP controls during annual financial statement audits, but these aren’t enough for ongoing compliance. External audits happen infrequently and focus on financial accuracy rather than day-to-day operational efficiency.

What are the warning signs that your AP policy needs updating?

Several indicators signal that existing policies no longer serve organizational needs effectively:

- Frequent exception requests: When standard procedures require constant workarounds, the policy doesn’t reflect operational reality.

- Increasing processing times: Lengthening approval cycles suggests bottlenecks in workflow design.

- Rising vendor complaints: Suppliers raising payment issues indicate that policy requirements create friction.

- Control failures or fraud incidents: Security breaches reveal inadequate safeguards.

- Staff confusion about procedures: Repeated questions about the same topics indicate unclear policy language.

- System capabilities exceeding policy requirements: New technology may enable better processes than documented procedures allow.

Employee turnover in the AP department may also indicate frustration with cumbersome policies that make daily work unnecessarily difficult. Exit interviews can reveal whether policy burdens contribute to retention problems.

How can you gather feedback from stakeholders about policy effectiveness?

Regular feedback helps uncover practical issues that metrics alone may miss. Annual surveys of AP staff, approvers, and key vendors provide structured insights into policy strengths and weaknesses. Focus questions on specific pain points rather than general satisfaction scores.

Quarterly stakeholder meetings that bring together AP, procurement, department managers, and IT create space to discuss policy challenges and identify improvement opportunities. These discussions often reveal cross-functional issues that individual teams may not see on their own.

Informal feedback channels, such as an AP policy suggestion box or a dedicated email address, allow employees to report issues in real time instead of waiting for formal review cycles. Monitoring the volume and common themes of feedback helps prioritize policy updates and improvements.

What reporting mechanisms ensure ongoing compliance?

Automated compliance dashboards provide real-time visibility into policy adherence. The dashboard should track:

- Authorization limit violations

- Approval turnaround times

- Invoices paid without proper documentation

- Vendor master file changes

Exception reports that highlight unusual patterns (for example, sudden increases in payments to specific vendors) should trigger further review and investigation.

Monthly compliance reports for finance leadership summarize key metrics, open audit findings, and any policy violations during the period. For significant issues, the report should include a root cause analysis and a clear action plan to prevent recurrence.

System-generated alerts can notify management immediately when high-risk events occur, such as changes to vendor banking information, split purchases intended to bypass approval limits, or urgent payment requests that exceed established criteria. These real-time alerts allow for quick intervention before issues escalate.

How do accounts payable policies support risk management and compliance?

Strong accounts payable policies function as a critical component of enterprise risk management frameworks. Well-designed policies prevent financial losses, ensure regulatory compliance, and demonstrate control effectiveness to auditors and stakeholders.

How AP policies reduce fraud, duplicate payments, and unauthorized spend

Fraud prevention starts with clear segregation of duties. No single individual should control the entire payment process. Assigning different employees to vendor setup, invoice approval, and payment execution creates built-in checkpoints where fraudulent activity is more likely to be detected.

Duplicate payment controls help catch both unintentional errors and deliberate fraud. Requirements such as invoice number verification, automated checks against previously paid invoices, and monthly vendor statement reconciliations help identify duplicates before they result in losses. Policies should also require investigation when a vendor submits multiple invoices with similar amounts or dates.

Maverick spending is reduced through clearly defined authorization limits and purchase order requirements. When a purchase order must be created before goods or services are ordered, spending can’t proceed without proper approval and budget validation. Non-PO invoices should follow an exception process that includes additional review and higher approval authority to reduce the risk of misuse.

What role AP policies play in audit readiness and regulatory compliance

Comprehensive AP policies show that management takes internal controls seriously. Auditors assess these policies when evaluating the strength of the organization’s control environment. Clear, documented procedures demonstrate that controls are properly designed and communicated to the employees responsible for executing them.

Policies that require audit trails ensure that complete transaction histories are preserved and accessible. Retaining invoice copies, approval records, and payment confirmations provides the documentation auditors need to test control effectiveness. Organizations with strong documentation practices typically complete audits more efficiently and with fewer findings.

Regulatory requirements vary by industry and jurisdiction. Policies should address obligations such as 1099 reporting for U.S. vendors, sales tax calculation and remittance, international payment restrictions, and industry-specific procurement rules. Regular policy reviews help ensure new regulations are incorporated promptly, rather than identified during compliance audits.

How strong AP policies support SOX and internal control frameworks

Sarbanes-Oxley (SOX) compliance requires documented internal controls over financial reporting, and accounts payable is a key process subject to control review. AP policies form the foundation of SOX documentation by defining how transactions are initiated, approved, recorded, and reconciled.

SOX-related controls typically include the following:

- Clear approval hierarchies to prevent unauthorized transactions

- Segregation of duties to avoid single-person control

- Reconciliation procedures to ensure accuracy

- System access controls that limit who can perform sensitive actions.

Policies document these controls and assign responsibility for their execution and oversight.

Each year, management must assess the effectiveness of internal controls for SOX compliance. Policies define how controls are designed, while monitoring activities and audit results provide evidence that they operate as intended. Organizations with well-documented AP policies are better positioned to complete SOX assessments efficiently and with greater confidence in their results.

Frequently asked questions about accounts payable policies

Accounts payable policies should be detailed enough to ensure consistent execution, but not so rigid that they attempt to cover every possible situation. The main policy should clearly define standard procedures, while unusual or complex cases can be addressed through separate guidelines or escalated to management. The goal is to create policies that employees can quickly reference during daily work.

Rigid policies that prioritize control over practicality can strain vendor relationships through delayed payments and burdensome documentation requirements. Suppliers may increase prices, refuse to offer favorable terms, or decline to do business with organizations whose payment processes create excessive administrative burden. The most effective policies balance strong internal controls with reasonable processes that allow vendors to submit invoices easily and receive timely payment.

Effective enforcement combines preventive system controls, ongoing monitoring, and clear accountability. Built-in controls should block non-compliant transactions before they are processed, while exception reports and audits help identify issues that require review. Training ensures employees understand the requirements, and automated workflows guide them through the correct steps. Management must also lead by example to address failures promptly and avoid policy overrides unless there is documented justification and proper authorization.

Looking for a way to apply your AP policy in daily workflows?

See how Precoro helps teams automate approvals, manage invoices, and maintain financial control. Book a demo.

{kind=link}