What Is PPV? Purchase Price Variance in Accounting Explained

Learn how to calculate purchase price variance, interpret its accounting impact, and use it to maximize your company’s cost efficiency.

Financial efficiency, cost savings, and profitability are undoubtedly among the top priorities of upper management, regardless of a company’s industry. However, only 54% of CPOs claim they have achieved their cost-saving targets in 2025. One of the ways that procurement teams can improve this figure is by tracking and reducing the purchase price variance (PPV) metric.

In this article, we'll explain what PPV is, how accounting records it in financial statements, why variance matters, and how tracking this metric can benefit your procurement processes.

Keep reading to find out:

What is purchase price variance?

What PPV indicates

Why is purchase price variance important?

How to calculate purchase price variance

How is purchase price variance treated in accounting?

Why does purchase price variance occur?

How do you analyze purchase price variance?

How to forecast PPV

How to manage PPV

See what Precoro can do for your PPV

Frequently asked questions about PPV

With knowledge of PPV comes cost control

What is purchase price variance?

Purchase price variance is a financial metric used in procurement and supply chain management to assess the difference between the expected (also known as standard or baseline) cost of an item and its actual purchase cost. PPV measures the gap between what the company planned to pay for a product or service and what they actually paid.

Purchase price variance can be tracked for each separate purchase or for the total procurement spend over specific time periods—for instance, monthly, quarterly, or yearly. You can monitor price fluctuations with PPV, and if used correctly, this metric provides vital insights into the effectiveness of cost-saving strategies.

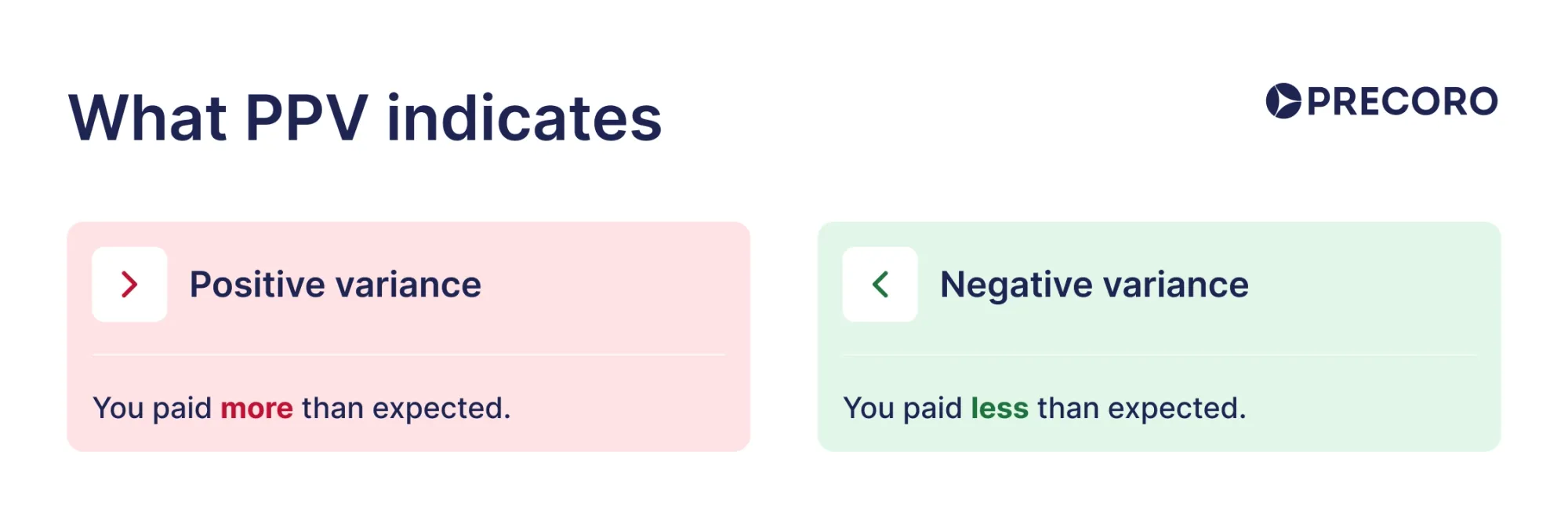

What PPV indicates

Purchase price variance is expressed as a number and indicates how well the company is managing purchasing cost-efficiency. PPV can be positive or negative; a positive variance means more was paid than initially expected, and a negative variance means less was paid.

Positive PPV, also known as unfavorable PPV, occurs when the actual price the company paid is higher than its anticipated price. A negative PPV, on the other hand, is considered favorable because the actual cost is lower than the budgeted cost.

Negative variance points to financial savings, but PPV alone isn’t enough to accurately assess procurement performance. Stakeholders shouldn’t chase negative PPV at any cost; rather, they should consider external factors and evaluate whether the company did the best it could in the current circumstances. After all, price volatility is sometimes out of the buying company’s hands. By focusing too much on the PPV metric, stakeholders might distort their other performance KPIs.

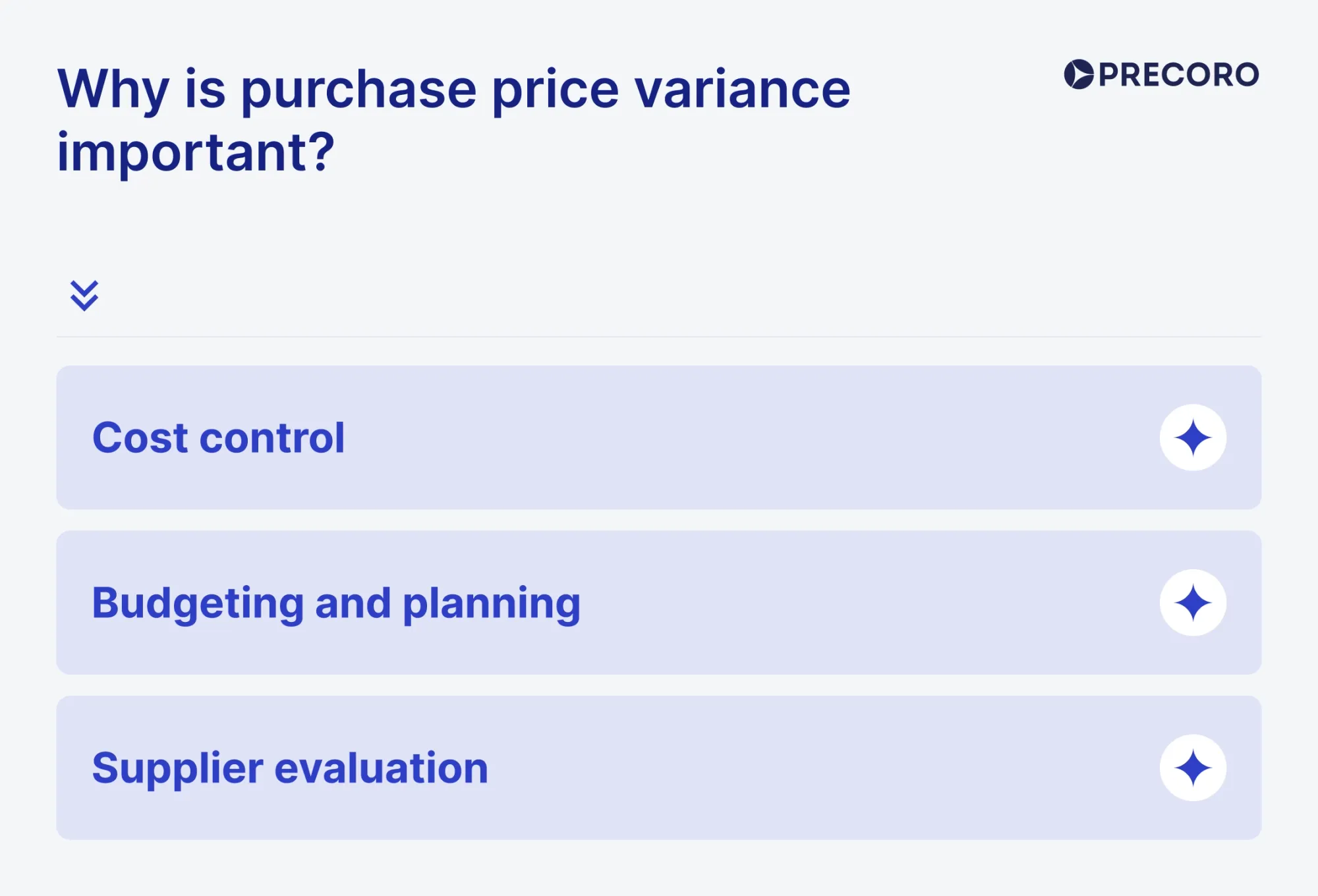

Why is purchase price variance important?

When suppliers charge more for the purchase than expected, the company spends more than initially planned, which directly impacts the budget and profit margins. That’s why keeping track of PPV is an important part of managing business costs that shouldn’t be underestimated.

PPV is still a key focus for any executive. In fact, improving profit margins via cost reduction remains among the top priorities of the high-performing CPOs. According to Deloitte’s Annual Global Chief Procurement Officer Survey 2025, it’s highlighted by 72% of CPOs, compared to 71% from 2023.

Stakeholders track purchase price variance to understand procurement spend and quantify its efficiency. The team can use it to evaluate current performance as well as for financial forecasting.

Cost control

Monitoring purchase price variance helps organizations identify cost overruns and underruns, so they can take corrective actions and control costs. By tracking PPV and addressing discrepancies, managers can ensure that the actual spending aligns with the budgeted costs.

Generally speaking, this happens in two ways: either you find a better price option, or you improve cost estimates with your existing supplier. In any case, managers with a good understanding of the current PPV and its tendencies can make informed decisions to control expenses.

Budgeting and planning

Purchase price variance is also a precise indicator of how accurate a company’s budgeting and financial planning are. When the company budget is created, the exact price for each purchase isn’t yet confirmed, so the procurement managers rely on estimated or standard costs based on forecasts and historical data. This estimate is then used as a standard price in the PPV formula.

After the company makes a purchase, procurement specialists can compare the actual cost against the budgeted cost. The smaller the variance of the purchase price, the more accurate the estimate was.

Supplier evaluation

PPV helps companies evaluate supplier performance. A consistent positive (unfavorable) variance could indicate issues with supplier pricing accuracy or even contract compliance. By analyzing PPV, procurement professionals can identify vendors who quote one price but invoice another and deliver goods or services at higher costs.

At the same time, PPV can be used to identify suppliers who consistently deliver products at or below the expected cost. Reducing orders from the former and increasing orders from the latter can seriously improve the company’s cost efficiency and lead to long-term savings and improved profitability.

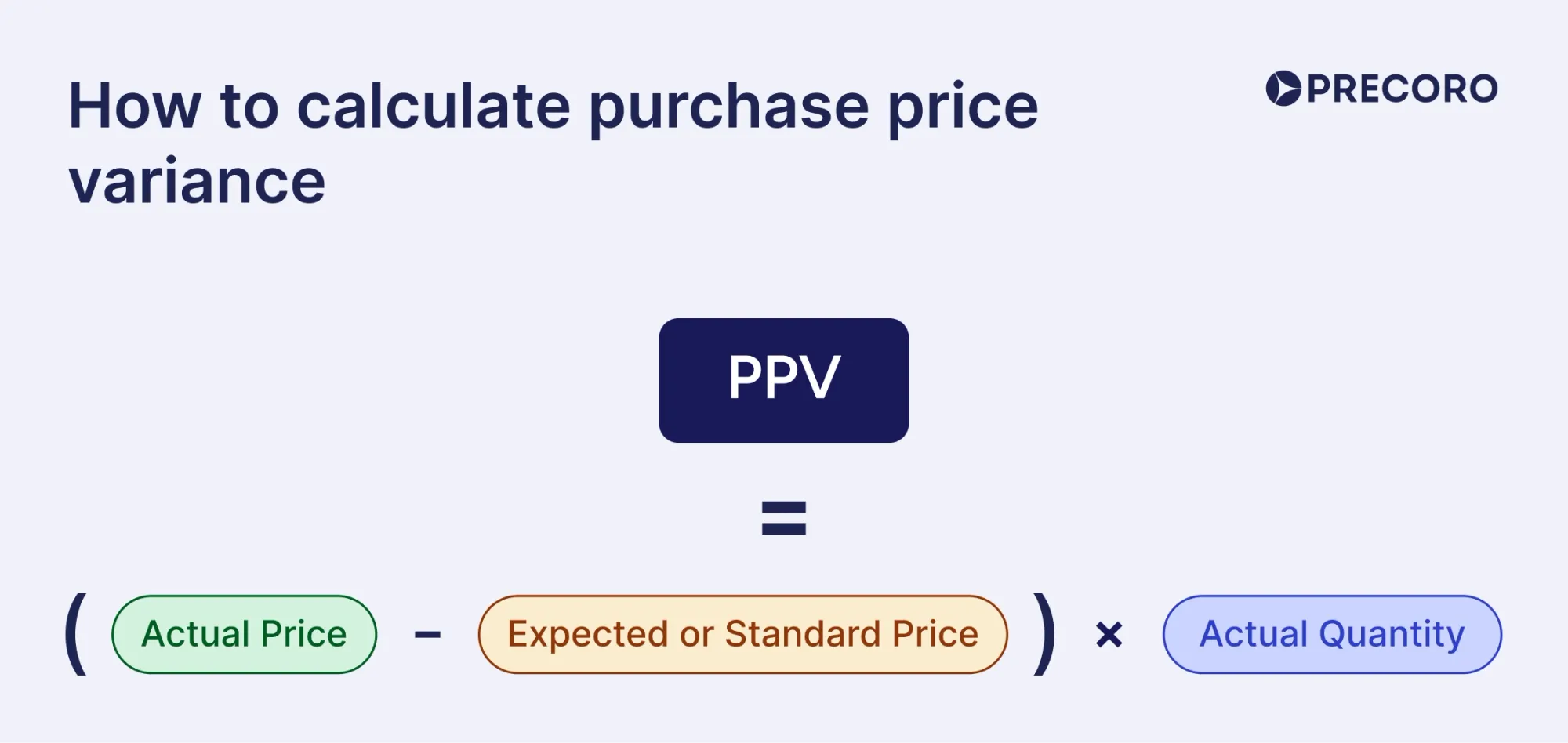

How to calculate purchase price variance

Purchasing professionals can calculate purchase price variance using a straightforward formula:

| Term | Definition |

|---|---|

| Actual Price | The real price paid for one unit of goods or services |

| Expected or Standard Price | The reference price your team planned to pay |

| Actual Quantity | The number of items or services purchased |

Actual Price refers to the price a company actually pays for a product or service. This number includes any additional charges that affect the actual unit cost, such as taxes and shipping fees.

Expected or Standard Price represents the budgeted price for the item before it is purchased. Procurement professionals estimate this figure during the budgeting process based on multiple factors: an average of historical prices (typically from the previous year to the current pricing), current market conditions, and supplier agreements.

Actual Quantity stands for the number of items or services purchased. It can be measured in any units relevant to your specific case, such as pieces, minutes, hours, kilograms, etc. Quantity must be considered in PPV calculations because it reflects the total financial impact of the price difference.

Even a small price change per item can deal a significant blow to your budget when applied to a large order. There’s also the matter of volume discounts, which usually change the price per unit once you hit a certain quantity.

Use this calculator to quickly determine how the price you’ve paid for goods or services compares to the standard price.

Purchase Price Variance Calculator

Calculate the difference between actual spend and budgeted spend.

How is purchase price variance treated in accounting?

Supply chain teams use PPV to determine how effective their purchasing is: whether supplier prices are still competitive, whether negotiated terms hold up, and whether current vendors remain viable at the prices they charge. It helps them answer questions like, “Are we still getting the right price from this supplier?” or “Should we renegotiate before the next order?”

Accounting teams, on the other hand, look at PPV from a different angle. Their focus is on the financial impact: how actual costs differ from budgeted or standard costs, where the variance should be recorded, and how it affects inventory, cost of goods sold, and profit.

How is PPV recorded in accounting?

PPV is primarily used in the standard costing method, which records purchases at the standard cost rather than what you actually paid. In this setup, the company compares the item's standard price to the actual supplier price. If the two don’t match, the difference is posted to a separate purchase price variance account.

In other costing methods, PPV may still be useful for procurement analysis, but it usually isn’t recorded as a separate accounting entry.

- Actual costing: Purchases are recorded at the real price paid to the supplier.

- Weighted average costing: The supplier price is blended with existing inventory costs to calculate a new average unit cost.

- Direct expense approach: For services or non-inventory purchases, the actual cost is usually recorded directly in an expense account or as COGS.

There’s usually no formal PPV record in these methods. Your team can still compare actual prices against standard or expected prices, but that comparison is mainly used for internal analysis, not accounting entries.

How is PPV handled in standard costing systems?

Standard costing is an accounting method used to compare the actual cost of production with the planned or expected cost for the same goods. The difference between what you expected to pay and what you actually paid is your variance.

In standard costing, the standard cost of the materials is debited to the inventory account, while the actual amount owed to the supplier is credited to accounts payable. The purchase price variance account acts as the balancing entry.

Positive or unfavorable variances are usually recorded as debits because they decrease the account balance, while negative or favorable variances are recorded as credits because they increase the account balance.

The general rule is:

- If the supplier charges more than expected, the variance is unfavorable and is recorded as a debit to the PPV account.

- If the supplier charges less than expected, the variance is favorable and is recorded as a credit to the PPV account.

For example, say your company receives materials with a standard cost of $24,000, but the supplier invoice later comes in at $25,800. The extra $1,800 is the positive purchase price variance, which is recorded separately.

| Account | Entry |

|---|---|

| Inventory | Debit $24,000 |

| Goods received not invoiced, or accrued liabilities | Credit $24,000 |

Once the invoice comes in, accounting records the actual amount owed to the supplier and separates the difference. GRNI now goes to debit since the actual invoice has already arrived. PPV is debited in a separate variance account to indicate the difference between standard and actual cost. The actual price is recorded in accounts payable.

| Account | Entry |

|---|---|

| Goods received not invoiced/accrued liabilities | Debit $24,000 |

| Purchase price variance | Debit $1,800 |

| Accounts payable | Credit $25,800 |

What’s the difference between standard vs. actual costing?

While standard costing records standard cost, actual cost, and PPV as separate entries, actual costing records goods at the real price paid to the supplier. So if the company expected to pay $10 per unit but paid $12, the system records the item at $12. There’s usually no separate PPV entry because the price difference is already included in the COGS or inventory value.

Neither method is automatically better since they serve different purposes. If you’re operating in a stable market with predictable price changes, standard costing provides a good baseline for variance analysis. In a volatile sector, however, actual costing helps keep inventory and COGS closer to real market prices, since supplier price changes are recorded as they happen.

Where does PPV appear in financial statements?

PPV usually appears first as a variance account in the general ledger. As the end of the financial period approaches, PPV can be transferred to a different account depending on the inventory status.

- Materials still in stock: PPV may be allocated to raw materials inventory on the balance sheet because the related goods haven’t been used or sold yet.

- Materials used in production but not sold: PPV may be allocated to work-in-process or finished goods inventory, depending on the stage of production.

- Products already sold: PPV usually moves to COGS, so the income statement reflects the actual cost tied to the revenue.

However, if the variance is small or turnover is quick, it might be more logical to move the entire PPV to COGS rather than split it across inventory accounts.

How do favorable and unfavorable PPV affect profit?

With a favorable PPV, the company paid less than planned. That difference translates directly into savings that boost your profit margins. An unfavorable PPV can reduce profit because the company paid more than expected. A sudden increase may force the company to dip into savings or stretch itself financially.

PPV doesn’t always affect profit right away. If the related goods are still in inventory, the variance may stay tied to inventory until those goods are sold. Once the goods move into COGS, the variance affects the income statement.

Why does purchase price variance occur?

Some reasons for the PPV are internal, while others are beyond the company’s control. Procurement specialists need to understand both to spot patterns and take appropriate actions to either minimize unfavorable PPVs or maximize favorable ones.

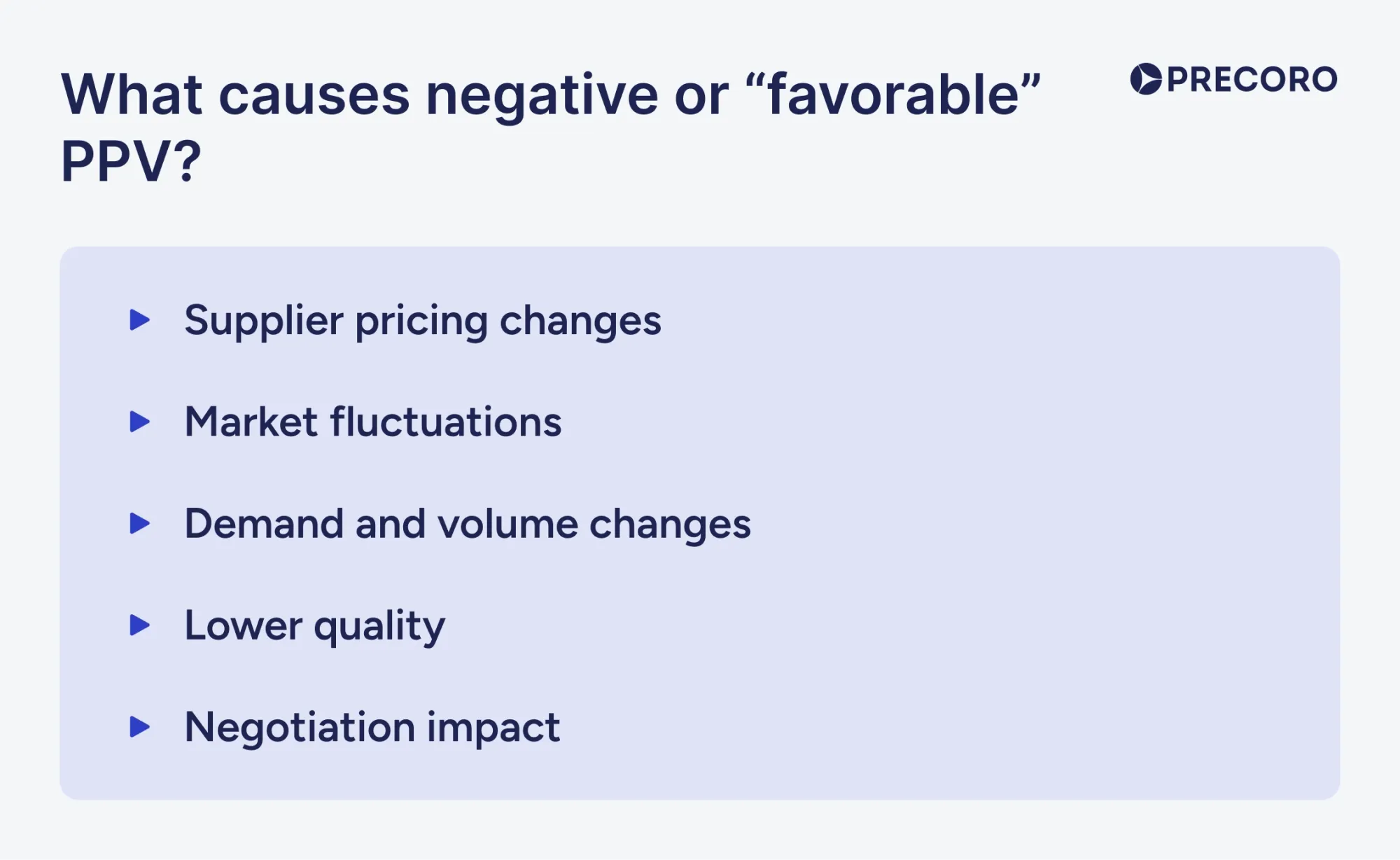

What causes negative or “favorable” PPV?

A negative purchase price variance (PPV) occurs when the actual price paid is lower than the budgeted or standard price. It’s considered favorable as the variance typically translates to cost savings for the company.

There are several typical reasons for a negative PPV. Some variances can be driven by decisions made by finance, procurement, or operations teams. Sometimes, external circumstances beyond the staff’s control also come into play.

Supplier pricing changes

Perhaps the biggest driver of favorable PPV comes from suppliers themselves, with little interference from the buyer’s side. Although the current trend is to raise prices, vendors may charge less than you initially expected. That favorable variance then saves the company more money and directly boosts profits.

Price reduction can happen when:

- Raw material costs or freight expenses dropped, so the final product is cheaper to produce.

- You qualify for a new discount tier (e.g., volume pricing, long-term partnership, etc.)

- The supplier offers promotional pricing for new customers, early payment discounts, or seasonal promotions.

- You renegotiate better terms or consolidate orders across the company.

- The vendor is pressured to do so because of market competition.

No matter the reason, the end result works in your favor—the supplier’s price is lower than the standard price, and the variance you get goes into savings. However, it’s important to remember that, unless these changes are embedded into the terms, you shouldn’t rely on them. Separate these occasional price drops from repeatable savings you can achieve through tactical negotiations and strategic sourcing.

Market fluctuations

Market shifts are a key external factor to consider when budgeting or estimating the standard cost of supplies. The market price of some raw materials or services might drop due to factors outside of the company’s control, such as shifts in demand or changes in global supply conditions.

Let’s remember, for example, how the prices for travel services dropped during and immediately after the COVID-19 crisis as demand decreased. Aluminum prices also reached new highs in 2022 and experienced a sharp decline in the following year due to lower demand. In both cases, buyers who closely monitored the market could take advantage of these volatilities and purchase goods or services at lower prices than expected, leading to favorable variance.

Demand and volume changes

When demand goes up, procurement can sometimes use that to its advantage. For instance, larger orders often unlock volume discounts or better terms from vendors once you reach a certain quantity threshold.

The same logic applies when teams consolidate purchases across departments or locations. The price for a single standalone order might be higher than if several orders were combined into a larger one. If your standard price was based on a smaller order, but you end up buying enough to get a lower price, that gap becomes favorable PPV. However, note that this only works if procurement is organized enough to plan and consolidate those orders.

Negotiation impact

Both demand and volume changes can be negotiated at the contracting level when you just begin the partnership. If procurement uses repeatable orders or consolidated demand as leverage, it can often get a favorable PPV.

Multi-year contracts are a good example of such a strategy. Rather than negotiate each order, the company commits to buying from the supplier over a defined period. In return, the supplier may offer lower unit prices, fixed discounts, rebates, or better pricing after certain volume thresholds are reached. For instance, a company might agree to purchase marketing consultancy services for 3 years with a 10% discount after the first year.

Lower quality

Lower product quality is also a reason for a lower actual price and, possibly, a favorable PPV. If the purchasing company is okay with the lower-quality alternative, they can proceed with the order and reap the benefits of negative PPV.

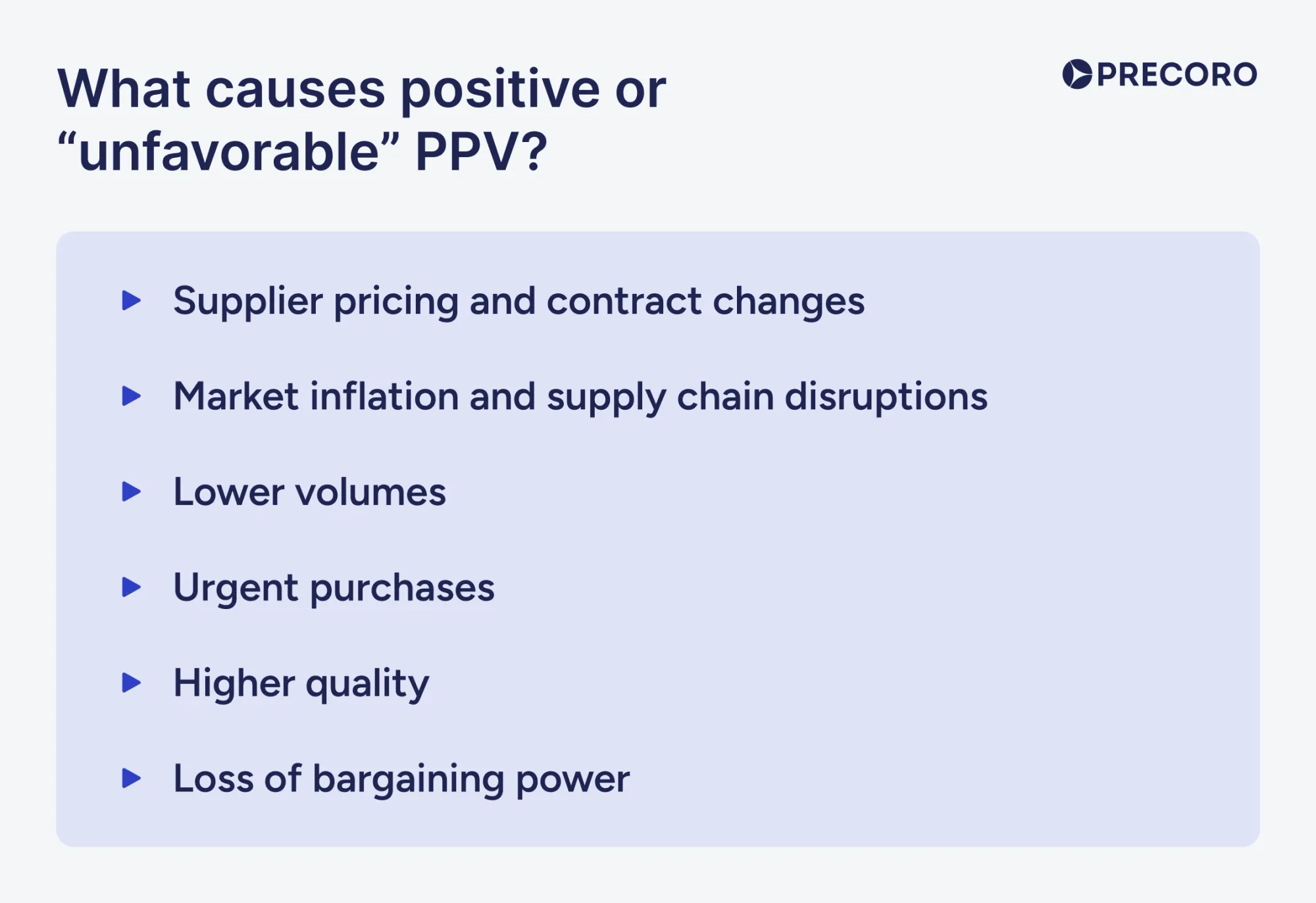

What causes positive or “unfavorable” PPV?

A positive variance indicates the company spent more than it expected, which can result in financial losses. It’s important to realize that positive variance doesn’t always mean there’s an issue with procurement management. An unfavorable PPV can simply mean the markets are shifting or supply chain disruptions are causing delays.

Supplier pricing or contract changes

Similar to how price drops can cause favorable PPV, any spikes in the cost of raw materials, freight charges, or general pricing structure will leave you with positive variance. The end of special pricing benefits can also lead to purchase price variance.

For example, the initial contract has expired, and the new one doesn’t offer discounts, or the selling company has stopped offering certain discounts altogether. These price fluctuations are often caused by changes in suppliers’ internal policies, so the buying company might not know how to account for them when preparing budgets.

Market inflation and supply chain disruptions

Market shifts are among the main reasons for unfavorable price variance. Supply chain disruptions and inflation can cause the costs of materials, goods, and services to go up. Actually, 59% of CPOs surveyed by Deloitte cited inflation as their top organizational risk.

These increased prices are often caused by factors neither the purchasing company nor the supplier can influence. Securing volume discounts, negotiating special deals, and maintaining strong supplier relationships can help minimize the negative effect of price fluctuations.

Lower volumes

Lower volumes can cause unfavorable PPV when purchases become too small or fragmented to support the price your team planned for. Instead of one larger order, the company may place several smaller orders across teams, locations, or projects. Each order then carries a higher unit price, extra handling fees, or worse delivery terms.

Urgent purchases

Maverick spend can also lead to unfavorable purchase price variances. When the company doesn’t implement necessary control practices, employees might make unapproved purchases in the company’s name that exceed the budget. Such purchases often include the most readily available items, selected for their delivery speed rather than cost efficiency.

Loss of bargaining power

A decrease in bargaining power can also result in unfavorable PPV. For instance, when a new buyer with higher purchasing power enters the market for scarce goods, demand for those goods increases. The supplier might no longer need to offer the favorable purchasing conditions it previously offered, which could lead to higher prices.

Higher quality

Higher product quality offered by the supplying company can cause the price of goods to go up, thereby affecting PPV. The buying company then has to consider whether the upgrade is worth the cost hike or if it’s time to look for an alternative.

How do you analyze purchase price variance?

The PPV metric alone doesn’t reflect the entire picture. To see results, you need to dig deeper: into the root causes of variance, key parties, and whether it’s a one-off or a clear pattern. Once you have calculated the PPV, follow it up with the right tools, such as regular reports and performance metrics.

Which reports can you use to analyze PPV?

To understand the cause of PPV and how to fix it, you need to look at it from more than one angle. Variance alone tells only one part of the story, as does a single spend report. The procurement team needs to combine several reports with supplier behavior, category trends, and the overall spend picture to get the full context.

During PPV analysis, the following insights can be useful:

- Spend reports show exactly how much the company spends across departments or time periods. They help you see where PPV has the biggest financial impact and if that impact warrants additional action from the company.

- Supplier reports break down purchasing data by vendor. With these findings, you can focus on specific suppliers and spot the key drivers behind variance: who charges above expected prices and where terms have changed. From there, you can choose which partnerships are worth renegotiating.

- Category reports group purchases by spend type, such as packaging, raw materials, IT, etc. You can identify categories at risk of unfavorable PPV or those that experience it frequently. Any purchasing groups with fragmented spend or inconsistent pricing create perfect conditions for variance.

- Standalone PPV reports focus directly on the difference between standard or expected costs and actual prices. Not every procurement software includes them, but some ERPs do. Your team can track favorable and unfavorable variance by item, supplier, quantity, and period.

Manually compiling the reports above will take hours, if not days, out of the procurement team’s week. That’s one of the reasons why procurement software has grown in popularity. Such tools centralize all purchasing data and automate tasks that take up your valuable time. Take Precoro, for instance. With its custom reports, teams can build insights around the points that matter the most for PPV, such as supplier, item, or category.

What KPIs should you track alongside PPV?

PPV alone doesn’t exactly explain why the actual cost differs from the expected cost. However, by tracking supporting KPIs, you can both quickly understand the key reasons and evaluate the performance of suppliers or your purchasing structure.

PPV amount and percentage

The PPV amount shows the direct financial impact. The PPV percentage, however, indicates how large the variance is compared to the expected cost. A drastic variance for one purchase might seem minor in other cases.

For example, a $5,000 unfavorable variance on a $20,000 order is 25% above the standard price. That same $5,000 variance on a $500,000 order translates only into 1% over the threshold, which is much less urgent.

Contract compliance rate

Track how often purchases follow negotiated supplier terms with the contract compliance rate. If you notice low compliance and unfavorable PPV, these two might be directly related. Perhaps, supplier pricing isn’t at fault; instead, employees might purchase off-contract or even ignore contract terms.

Maverick spend rate

Maverick spend rate indicates the percentage of purchases made outside approved procurement channels or contracts. Off-contract purchases often come with higher prices, so a high maverick spend rate can explain why PPV is unfavorable. If such instances are frequent, it’s worth tracking them regularly and analyzing which areas they happen in.

Budget variance

Budget variance shows how actual spend compares with the approved budget. PPV explains price differences, but budget variance shows the broader financial impact. A company may have a favorable PPV but still exceed budget because it bought more than planned. Or it may have an unfavorable PPV but still stay within budget because the total demand was lower.

Realized savings

Realized savings measure whether favorable PPV turned into actual, repeatable savings. A lower price can result from a one-time market drop, a temporary promotion, or a genuine negotiation breakthrough. Tracking realized savings helps procurement separate lucky decreases from savings the company can expect again.

| KPI | What it measures | Calculation |

|---|---|---|

| PPV amount | The total financial impact of the price difference | (Actual price − Standard price) × Actual quantity |

| PPV percentage | How large the variance is compared to the standard price | PPV amount ÷ (Standard price × Actual quantity) × 100 |

| Contract compliance rate | Whether the teams are buying at negotiated prices | Contract-compliant purchases ÷ Total purchases × 100 |

| Maverick spend | The number of purchases made off-contract | Off-contract spend ÷ Total spend × 100 |

| Budget variance | How actual spending differs from the budget | Actual spend − Budgeted spend |

| Realized savings | The actual savings achieved after purchase | No universal formula. Compare actual spend with expected spend and verify whether the savings were actually captured |

How often should you review purchase price variance?

For best results, purchase price variance should be reviewed at least monthly, together with the month-end close statements. This system works for most teams since it aligns with the traditional accounting cycles and remains regular enough to spot any pricing changes or repeated variances. For high-risk categories, such as raw materials, you can review them biweekly to spot volatility in time.

Review PPV quarterly when the company is ready to make more strategic decisions. Flag any suppliers or categories that need renegotiation during monthly reviews and use quarterly ones to focus on broader spend patterns and supply chain impact.

How can you reduce unfavorable PPV?

If unfavorable PPV appears often, the root cause might go deeper than just the supplier changing their prices. Sometimes, either the standard price is no longer realistic or the method used to estimate it needs a second opinion.

Before taking any drastic action, realign the costs you’re paying for supplies with the expected price. Look at the percentage and frequency of the variance. If it’s large and continues to occur, reconsider your approach to calculating expected prices. After that, utilize the following practices.

1. Approach supplier negotiations strategically

Treat negotiations as part of PPV control and enter them with clear numbers. Review past prices, annual spend, and supplier performance for that category, and decide what exactly your team wants to get out of this discussion.

- Lock down prices with contracts. If the price isn’t fixed in the contract, there’s always a chance that it’ll change during the next purchase, directly contributing to an unfavorable PPV. Negotiate a fixed deal in which the cost remains the same for a set period, such as several months or a year.

- Aim for volume discounts. Look into suppliers who offer volume-based discounts. In this case, the cost will be lower per unit, and the unfavorable PPV will therefore also drop. If you’re already working with a supplier you want to continue the partnership with, inquire about tier discounts. For example, the vendor charges one price for 1-500 units and a lower price for 500-1,000 units.

- Ask for rebates. To entice customers, some suppliers offer rebates, returns of a certain amount of money after purchase, which are often offered once you pass a certain purchasing threshold. This sum can directly boost your PPV and contribute to profits.

- Challenge price increases. Whenever the supply cost increases, ask the supplier to explain what changed to warrant the higher price. Compare their claims with your data, and if they don’t hold up—or there’s no clear explanation—push for a lower cost or consider switching vendors.

- Compare supplier quotes. If the price increases, assess the state of the supply market and review related suppliers. Assess whether the price you’re currently paying aligns with the market average and how the quality of goods and services justifies the price.

The above practices only work if you do them regularly, not once a year. Set a dedicated time for the team to go over any variances, discuss their root causes, and how you can mitigate them in supplier negotiations.

2. Practice strategic sourcing

Strategic sourcing is one of the most important causes of a favorable price variance and, therefore, can help reduce unfavorable PPV. When procurement managers are strategic about supplier research and screening, there’s a much higher chance of signing a contract with a vendor that guarantees a good offer and reliable conditions.

Strategic sourcing takes into account not only the immediate benefits of the offer (usually a lower price) but also considers the big-picture gains, such as discounts or delivery methods. For instance, choosing a supplier with flexible delivery capacities gives a purchasing team opportunities to consolidate orders and can result in reduced overall shipping costs, lower total cost per unit, and a favorable PPV.

3. Use volume purchasing with care

Volume purchasing, or purchasing consolidation, can reduce unfavorable PPV by giving your company stronger buying power. With some suppliers, a higher quantity leads to a lower cost per unit. The benefits are undeniable—you pay less for more, and PPV is also lower, to the point where it almost seems insignificant.

The company, however, has to accept some trade-offs. A higher quantity entails higher delivery costs, additional inventory expenses and space, and even the risk that materials or services will go obsolete. Unless you’re completely confident that these supplies will be used within a certain timeframe, these costs will still resurface in the form of unfavorable PPV, just later during the material lifecycle.

Focus on stable, low-risk categories with predictable demand and long shelf life. Carefully calculate where the materials will be used and how, so that excess stock won’t clog your inventory.

4. Strengthen your contracting approach

Contracts seem like a natural safeguard against unfavorable PPV simply because they’re fixed, long-term agreements. The price is locked in, so how can variance still leak into your orders? What many companies forget is that terms only deliver on the benefits they promise after they’re actually enforced. Here’s what your contracting approach should include to keep unfavorable PPV as close to zero as possible.

- Fixed pricing: The exact price the supplier will charge for a specific period. Including it in a contract ensures your PPV remains stable for the duration of the partnership.

- Price adjustment clauses: Terms that define when the supplier can change prices and how much notice they should give before doing so. That way, the company knows when to expect an increase and can adjust the budget accordingly.

- Volume tiers: Thresholds that include volume-based pricing once you hit a certain quantity. This approach can help mitigate unfavorable PPV.

- Catalog pricing: Approved catalogs with negotiated pricing. If it’s embedded directly into your purchasing system, whether it’s an ERP or procurement software, employees can purchase at the agreed-upon prices from the start without going off-contract.

- Centralized contract management system: A single place to store supplier contracts, pricing terms, renewal dates, and related documents. It helps procurement and finance quickly check what was agreed, which prices apply, and whether purchases comply with the contract.

- 3-way matching: A process that compares the purchase order, receipt, and invoice before payment. If the invoice price is higher than the PO price, the AP team flags the mismatch before the company pays and before the variance even happens.

- Performance SLAs: Supplier service commitments for delivery times, quality, response speed, and issue resolution. They help make sure lower prices don’t come with hidden costs, such as late deliveries, defects, urgent replacements, or extra manual work.

- Review schedule: A planned timeline for checking contract prices, supplier performance, rebates, volume tiers, and market changes. Regular reviews help keep expected prices accurate and prevent outdated contract terms from causing recurring PPV issues.

- Total cost of ownership: The full cost of working with a supplier, not just the unit price. It includes freight, storage, maintenance, defects, delays, payment terms, and other costs that affect the purchase's true value.

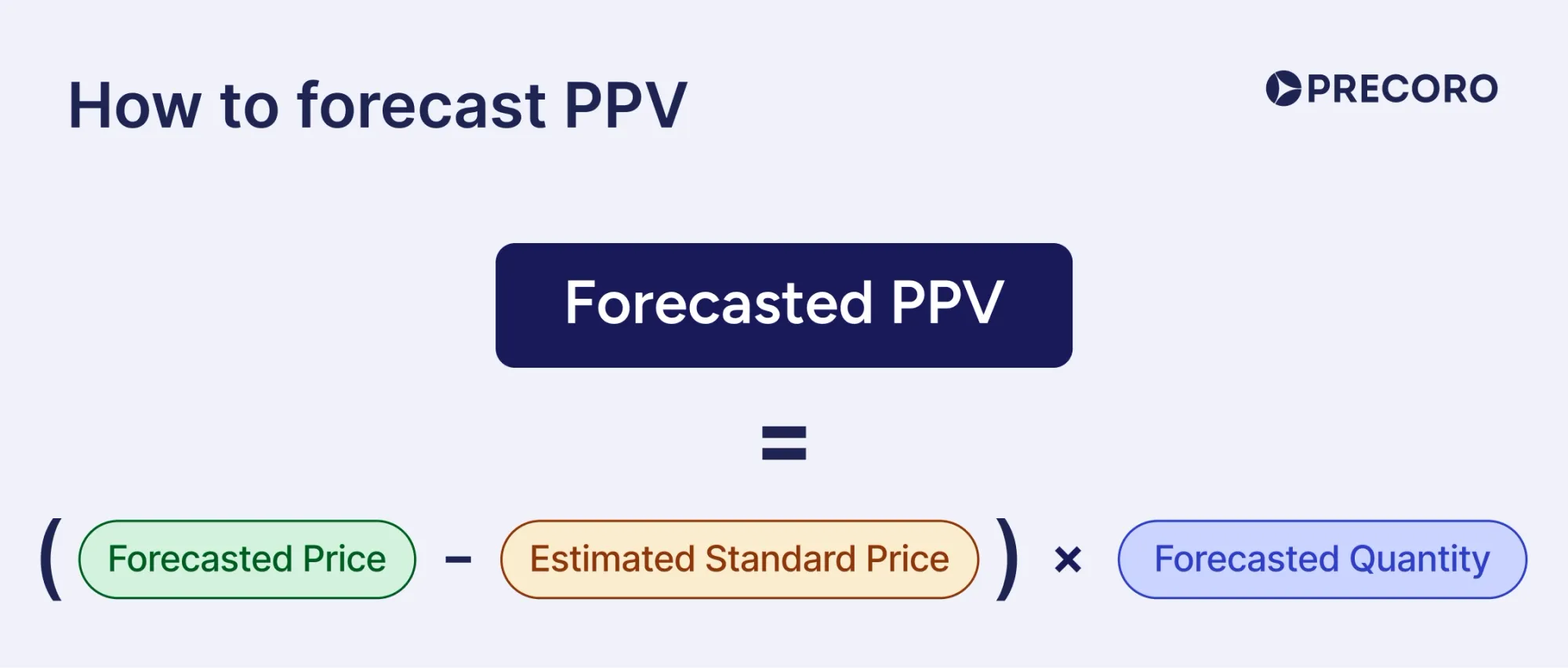

How to forecast PPV

While purchase price variance is a historical indicator used to assess completed purchases, companies can also predict it ahead of time before transactions happen. You can forecast PPV: even if the results won’t be completely certain, your team can use these metrics to check whether the expected prices match your planned spend before any purchases are finalized.

PPV forecasting helps companies evaluate how possible price changes can affect their future cost of goods sold and gross margin. It can also highlight the future financial risks for the business. This is especially true for manufacturing companies that need to carefully plan direct material purchases, as their profitability is highly dependent on raw material costs.

Business stakeholders can prepare PPV forecasts by analyzing historical pricing data, finding the price development patterns, and applying them to the current market situation. It’s also worth estimating the best and worst possible scenarios so businesses can be prepared for anything.

The procurement team can calculate forecasted PPV with a formula similar to that of historical PPV:

| Term | Definition |

|---|---|

| Forecasted Price | The price you expect to pay for a product or service |

| Estimated Standard Price | The expected price for an item at the time of purchase |

| Forecasted Quantity | The amount of goods or services you plan to purchase |

Forecasted Price stands for the price the business expects to pay for the goods or services. When determining this number, specialists should consider all possible scenarios that could affect the final cost, such as different delivery options.

The estimated standard price represents the expectations for the standard purchase price of the goods and services at the given moment on that specific market. To evaluate this number, analysts ought to consider market conditions and inflation.

Forecasted Quantity is the volume of goods or services that the company plans to buy. Depending on the actual production needs, order quantity can change and affect whether the company qualifies for specific offers and discounts. Forecasted quantities are usually based on expected market demand, production planning, and historical quantities.

Since many factors can affect the price of goods and services, forecasted purchase price variance is rarely about one fixed number. It’s usually a range of possible outcomes, with some scenarios more likely than others.

Use this calculator to forecast your PPV before it affects your budget.

Forecasted PPV Calculator

Estimate how future price changes could affect planned purchasing costs.

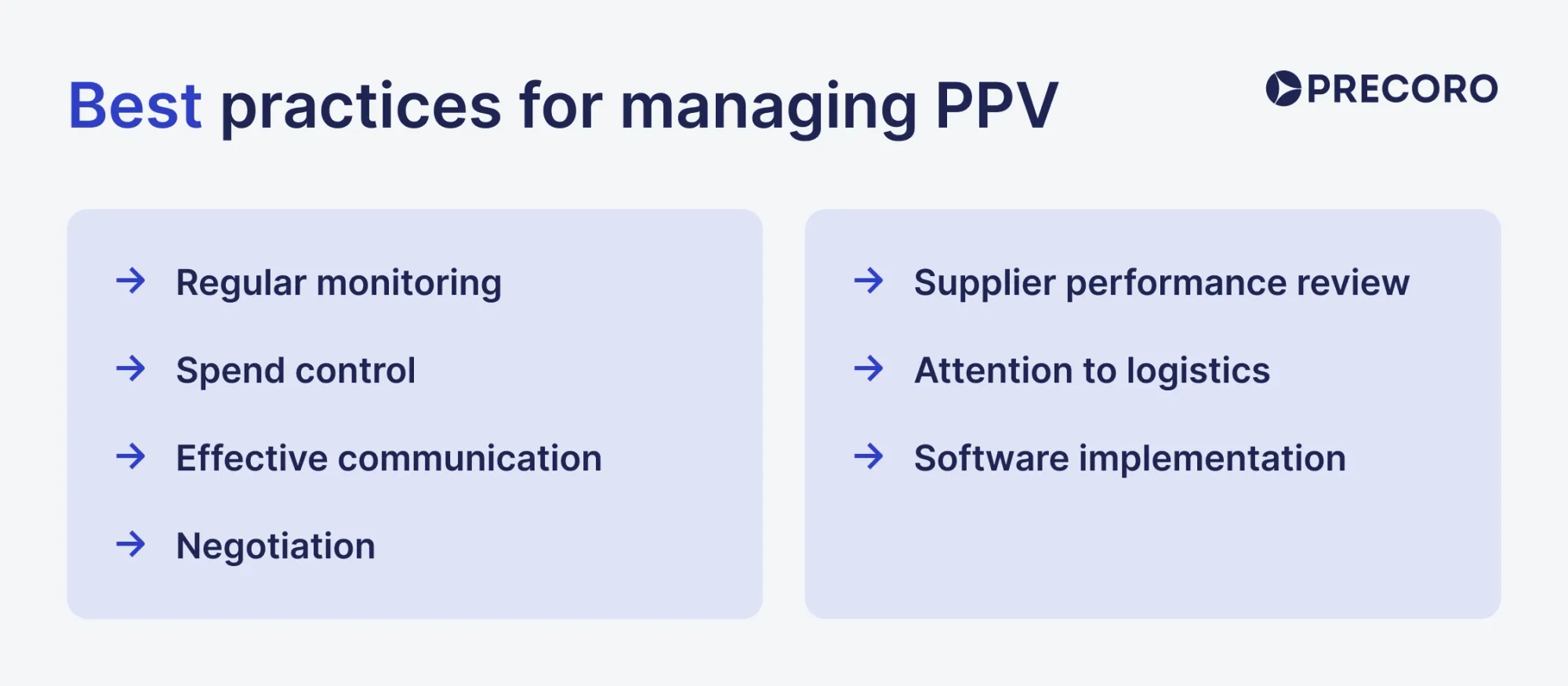

How to manage PPV

Managing purchase price variance isn’t straightforward, and stakeholders need to consider all factors that might affect it. For instance, a company can achieve a favorable PPV by ordering a large bulk of products from the vendor and qualifying for a quantity discount. But if the company orders more than it can use in time, the business will face the risk of excess inventory and growing storage expenses.

Simply reducing the price-per-item isn’t a surefire way to achieve favorable PPV. Here are some other methods to balance PPV metrics.

Regular monitoring

Implement regular reporting and continuously monitor PPV to catch discrepancies as soon as possible. Document transparency and easy access to purchasing data enable purchasing managers to achieve greater spending visibility. The sooner the purchasing team identifies a significant variance, the quicker they can take corrective action.

Spend control

Establish company-wide spend practices and implement approval workflows to achieve purchase visibility and control tail and maverick spend. When everyone involved in the purchasing process understands the approval process, it’s easier to ensure employees purchase the required items from authorized suppliers.

Effective communication

Set up a system for clear communication between the procurement and finance teams. Collaboration between these teams is crucial for maintaining accurate cost estimations and preventing discrepancies before placing orders. You can also introduce standardized templates and common terminology for employees who create documents.

Ensure teams across all relevant departments are aware of the procurement workflow and have a system that keeps them up to date on their documents. This way, everyone involved in processing and paying for orders will be aware of the price developments at any given moment.

Negotiation

Negotiate with suppliers to secure favorable and stable pricing terms. Regular reviews of supplier contracts and maximizing offers like volume discounts can lead to favorable purchase price variances.

Supplier performance reviews

Conduct regular reviews of supplier performance, and use purchase price variance as a metric to assess supplier consistency. By evaluating supplier performance in relation to PPV, you can make data-driven decisions about whether to extend or renegotiate contracts.

Attention to logistics

Delivery and storage costs constitute a substantial part of the total purchase cost. These components are often overlooked as the procurement team focuses on finding the items at the best price.

Companies should also plan ahead, consider the delivery routes, and prepare to mitigate any shipping risks. Plus, they should strive to keep inventory at an optimal level; overstocking adds to the overall item price due to storage costs, while emergency purchases can be costly because of express shipping.

Software implementation

Implementing procurement software can significantly improve transaction efficiency, supplier management, and data accessibility. Procurement software serves as a centralized platform for managing all procurement-related data, including pricing agreements and purchase orders.

With accurate and up-to-date data readily available, it's easier to calculate standard costs and track actual spend. Such software enables real-time monitoring of purchasing activities and actual prices and can alert users to significant pricing deviations.

With specialized software, companies can automate procurement workflows by defining steps and assigning specific users to each stage. By sending all procurement paperwork through predefined approval workflows, companies ensure that each document meets all requirements before advancing to the next stage, and that the price is approved before any order is placed.

Three-way matching is also easier within a digital solution that fully automates the comparison of POs, invoices, and receipts, minimizing errors. Procurement teams can easily identify unfavorable pricing in time to fix it before it’s approved and paid.

Procurement software also makes it easier to work with the numbers. Tools like Precoro centralize purchasing and supplier data, provide easy access to spend details via an AI Assistant, and generate reports for stakeholder meetings. Contact us at Precoro to learn how procurement software can improve your purchasing experience and maximize favorable purchase price variances.

See what Precoro can do for your PPV

Purchase price variance is much easier to control when you can see the details behind each price: what was requested, who approved it, which supplier was selected, and the agreed price. Nothing provides better visibility and control than Precoro, which brings all of these together in a single connected workflow.

Catch price differences before payment

Precoro connects purchase orders, receipts, and invoices, then helps teams match them before payment. The platform automatically performs 2-way and 3-way matching and flags discrepancies between POs, invoices, and receipts. That directly changes your PPV strategy. Rather than finding out the variance after the invoice is paid, your team can spot when the invoiced price doesn’t match the expected PO price early on.

Compare expected prices with actual spend

PPV analysis depends on clean purchase data. Precoro gives teams visibility into what was bought, where, when, by whom, and at what price. Compare planned pricing against actual supplier charges across departments, locations, and suppliers.

You can also pull custom reports by document, supplier, category, budget, or location. This functionality is useful for an in-depth PPV analysis, during which you need to review price changes at the category or supplier level.

Link negotiated pricing to the actual purchase

Unfavorable PPV often happens when teams buy outside of agreed-upon terms or use outdated supplier pricing. Precoro guides employees to approved suppliers via PunchOut or item catalogs, and links each PO and invoice to its related contract. Track contract amounts, monitor spent and available balances, and receive notifications when the purchase exceeds the limit.

Use supplier and category data to find patterns

One price mismatch may be a simple mistake, but several occurrences already point to a bigger issue. Precoro’s reporting lets teams analyze procurement data across POs, invoices, receipts, suppliers, contracts, payments, and stock transfers, with 150+ data points available for deeper spend analysis. For quick answers, your personal AI assistant is always on standby with in-depth replies.

With this toolkit, you can quickly understand:

- Which suppliers cause the largest unfavorable variance?

- Which categories are most exposed to price changes?

- Which locations pay more for the same items?

- Which contracts are close to expiration or over their limits?

- Where can we consolidate purchases to improve pricing?

Consolidate purchases to secure better rates

Precoro helps teams consolidate buying, prevent duplicate orders, and secure more favorable pricing. Companies with distributed teams or locations can see demand across the entire business and combine multiple purchases into a single order for a lower PPV and better pricing.

Frequently asked questions about PPV

In purchasing, PPV stands for purchase price variance. It’s a financial metric used in procurement and supply chain management to assess the difference between the expected cost of an item and its actual purchase cost. Based on PPV, purchasing teams can see where supplier prices, negotiated terms, or market changes caused costs to come in higher or lower than planned.

PPV measures the gap between what a company planned to pay for a product or service and what they actually paid. Purchase price variance can be tracked for each separate purchase or for the total procurement spend over specific time periods.

Purchase price variance can be calculated with a straightforward formula: PPV = (Actual Price — Expected or Standard Price) x Actual Quantity.

Purchase price variance is usually recorded in a standard costing system. Inventory is recorded at the standard cost, while the difference between the standard price and the actual supplier price is posted to a separate purchase price variance account. If the actual price exceeds the standard price, the company records an unfavorable PPV. If the actual price is lower, it records a favorable PPV.

Purchase price variance compares the actual purchase price with the standard price. It shows whether the company bought goods or services for more or less than planned. Invoice price variance compares the invoice price with the purchase order price. It shows whether the supplier charged a price different from the one approved on the PO.

With knowledge of PPV comes cost control

Understanding and managing purchase price variance is essential for controlling costs, evaluating suppliers, and improving profitability. By keeping a close eye on PPV and taking appropriate actions, the procurement team can optimize procurement processes and ensure cost-efficiency is prioritized when planning purchases and placing orders.

Effective PPV management requires vigilance, continuous data analysis, and collaboration across different departments. By consistently monitoring and analyzing this financial metric, the procurement team can make informed decisions that lead to cost savings and increased profitability.

See what Precoro is capable of

{kind=link}