29 min read

AP Automation and Global E-Invoicing Mandates for 2026

Learn how to survive global e-invoicing mandates across key regions and how to stay compliant and efficient with AP automation.

You can’t just stand and watch your team manually handle AP and AR. Let the manual processing of e-invoices rest in the past. Especially under Continuous Transaction Controls, tax authorities no longer just review transactions — they participate in them. In many systems, invoices are vetted, approved, or rejected before they even reach the buyer. What was once a back-office task is now a real-time coordination challenge between business and government.

From Italy’s SdI and Poland’s KSeF to ZATCA (Saudi Arabia) and the global Peppol network, finance teams are navigating a live, fragmented compliance web that determines whether a transaction can move at all.

More than 80 countries have implemented e-invoicing mandates, and 50 more plan to impose new or additional mandates.

This article explores different e-invoicing frameworks and how forward-thinking finance leaders manage not just to survive this regulatory tightening, but to turn compliance into a strategic data advantage.

Read more about:

What are global e-invoicing mandates?

Post-audit vs. clearance models: What’s the difference, and why is there a shift?

What is Peppol?

The 2025-2026 global e-invoicing map

Why native ERP modules fail at global e-invoicing?

What are the penalties for non-compliance?

Benefits of mandatory e-invoices

How to prepare for e-invoicing compliance and mandates

Automate your AP process with Precoro’s e-invoicing solution

Frequently asked questions about global e-invoicing mandates & AP automation

Don’t let compliance fall behind because of e-invoicing mandates

- E-invoicing ≠ PDFs — it’s structured, machine-readable data (XML, UBL, JSON) designed for system-to-system exchange.

- Governments are becoming active participants in every transaction.

- Peppol is emerging as the global standard.

- E-invoicing is becoming unavoidable worldwide, with 2025–2027 as a major global rollout phase.

- Compliance can become a competitive advantage.

- ERP systems alone aren’t enough—companies need specialized e-invoicing and AP automation tools.

- Automate early or face costly, reactive compliance later.

What are global e-invoicing mandates?

Global e-invoicing mandates are government regulations that require businesses to issue and receive invoices in a structured electronic format (e.g., XML/UBL via Peppol or national platforms like France's PPF or Poland's KSeF).

Mandatory e-invoicing transforms how businesses manage invoices and interact with tax authorities worldwide. Many countries are adopting these mandates to improve tax compliance, reduce fraud, and increase efficiency in invoice processing and automated VAT reconciliation.

Many people confuse a "digital invoice" (like a PDF sent via email) with an "e-invoice." For a government mandate, a PDF usually doesn't count because a computer can't easily "read" the data fields. A true e-invoice is a data file designed for machine-to-machine communication.

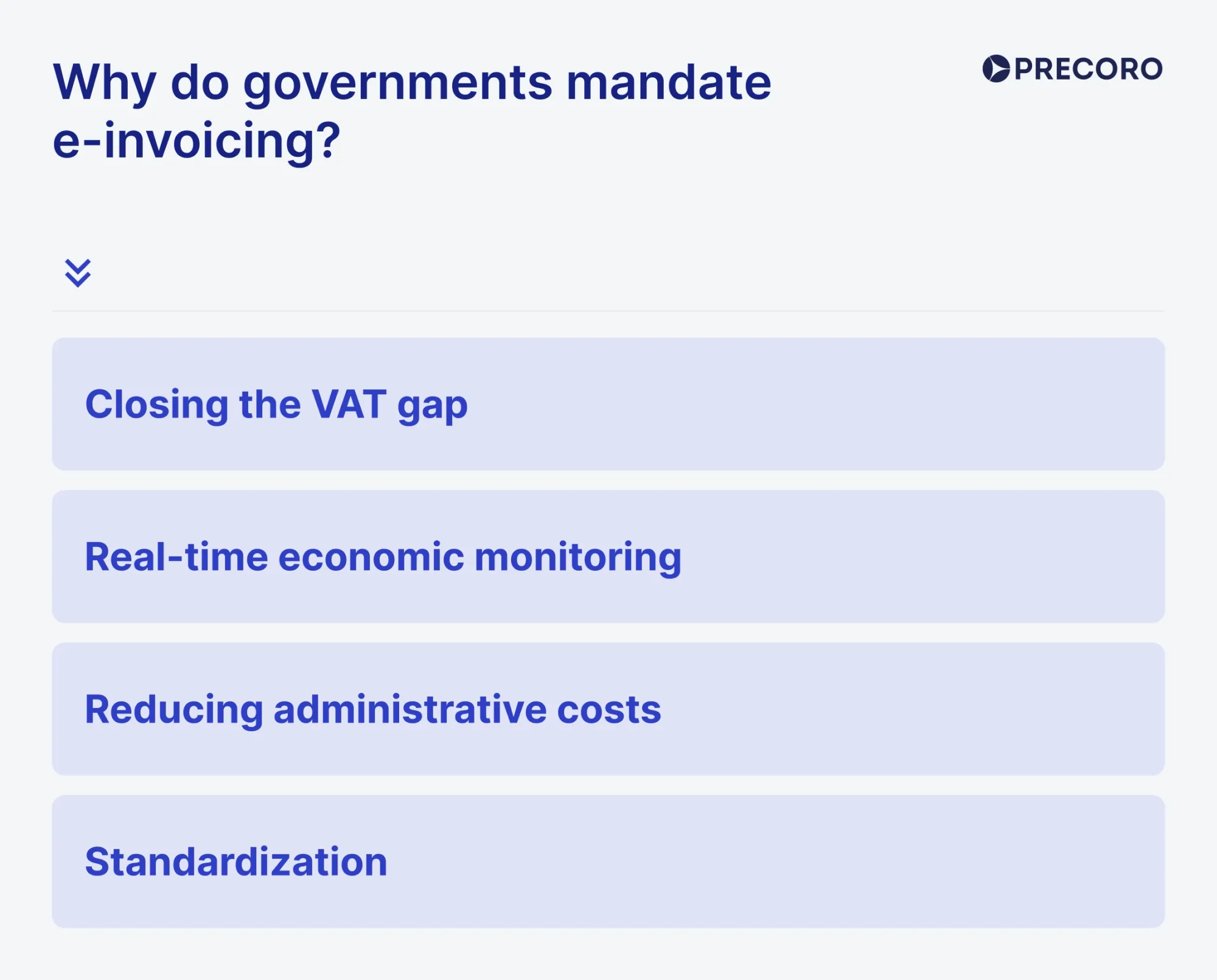

Why do governments mandate e-invoicing?

Governments mandate e-invoicing to reinforce tax compliance, prevent fraud, and gain real-time visibility into financial transactions. E-invoicing also supports digital transformation, improves economic monitoring, and decision-making.

Here are the key drivers behind these mandates:

Closing the VAT gap

The primary motivator for most governments is revenue protection. The VAT gap is the difference between the expected VAT (Value Added Tax) revenue and the amount actually collected. By requiring real-time reporting, governments can catch:

- Carousel fraud: Where businesses charge VAT but disappear before paying it to the government.

- Under-reporting: Ensuring the seller's reported income matches the buyer's reported expense.

Real-time economic monitoring

Traditional tax audits happen months or even years after a transaction. With e-invoicing, the government receives data in near real time, which allows them to:

- Monitor the "health" of the economy week-by-week.

- Identify industry-wide trends or sudden downturns instantly.

- Predict tax revenue with much higher accuracy.

Reducing administrative costs

While the initial setup is a hurdle for businesses, the long-term goal is a more efficient economy. E-invoicing helps by:

- Reducing manual entry and errors: Fewer manual inputs lead to faster payments.

- Pre-filling tax returns: In many countries (such as Chile and Italy), the government uses e-invoice data to pre-fill VAT returns for companies, saving hours of accounting work.

- Faster payments: Digital systems speed up the verification process, helping SMEs maintain better cash flow.

Standardization

Without a mandate, companies use different formats like PDF, CSV, and Excel spreadsheets that don’t work well together. E-invoicing mandates enforce a common standard (such as Peppol), ensuring invoices can be automatically processed by different systems without manual work.

What are e-invoicing standards?

E-invoicing rules are set by tax authorities or public bodies and define how invoices must be formatted, sent, stored, and reported. While they vary by country, most follow the same core requirements:

| Component | Description | Purpose & examples |

|---|---|---|

| Structured formatting | Machine-readable formats like XML, UBL, or JSON (e.g., EN 16931 in the EU). | Enables automation; Peppol BIS 3.0 for cross-border, India's JSON for GST. |

| Government clearance | Pre-submission to portals for validation (clearance model). | Fraud prevention; Brazil's SEFAZ or France's PDP from 2026. |

| Required fields | Tax IDs, invoice number, dates, line items, tax amounts, and totals. | Rejects invalid invoices; 20+ fields in Poland's KSeF. |

| Reporting | Real-time/periodic data to authorities (CTCs or e-reporting). | Visibility for audits; EU ViDA by 2030, UAE portals. |

| Storage | Digital archiving for 5–10 years, searchable and secure. | Legal retention; 10 years in Germany with indexing. |

| Authentication | Digital signatures, e-seals, or certificates. | Tamper-proofing; mandatory in Italy's FatturaPA. |

Post-audit vs. clearance models: What’s the difference, and why is there a shift?

In the post-audit model, businesses issue invoices independently without prior submission to tax authorities. They may later request and review these invoices to verify AP automation compliance and accuracy.

By contrast, in the clearance model, invoices must be approved by the tax authority first before they are sent. This approach gives more control and fewer mistakes, but it costs more upfront and can slow things down.

What is the post‑audit model?

The post‑audit model is a traditional model of tax supervision (especially for VAT) in which the tax authority stays out of a business’s day‑to‑day operations and only verifies compliance after transactions have been recorded.

In this system, the “audit” happens retrospectively, often months or even years after a transaction. The authorities may later request and review the underlying invoices to verify that the reported tax figures match the actual business activity. It therefore relies heavily on the taxpayer’s honesty and the accuracy and integrity of their internal record‑keeping.

This model offers greater flexibility and relies on periodic audits, with lower upfront compliance costs but a higher risk of penalties if issues are identified. It also requires thorough and reliable invoice storage.

How does the post‑audit model work?

The flow of information is direct and private between the two parties involved:

- Transaction: A seller provides goods or services to a buyer.

- Invoicing: The seller issues an invoice (paper, PDF, or electronic) directly to the buyer, without sending it to the tax authority in real time.

- Archiving: Both parties are legally required to store the invoice for a set retention period (typically 7–10 years) so that the tax authority can request it later if needed. The business must also ensure that the invoice remains authentic and unaltered (for example, by applying digital signatures or secure internal controls where required).

- Reporting: At the end of a tax period, the business summarizes all its invoices and related data in a structured tax or VAT return and submits it to the tax authority.

- The audit: If the tax authority notices a discrepancy or performs a random check, it requests the archived invoices and supporting records. It then verifies that the figures on the tax return match the underlying transactions and that the invoices haven’t been tampered with.

What is the clearance model?

The clearance model is a modern tax compliance system where the government acts as a "gatekeeper" for every transaction. It requires tax authorities to validate or "clear" invoices in real time (or near real time) before they can be issued to buyers. This process involves submitting invoice data to the government platform at the point of transaction, often with three parties involved: the seller, the buyer, and the authority.

It features more control points, like Continuous Transaction Controls (CTCs), ensuring immediate compliance and full visibility into economic activity. While this approach increases upfront costs and can delay transaction times due to validation, it minimizes fraud risks and errors by catching issues proactively.

How does the clearance model work?

The process moves in a specific, mandatory sequence:

- Creation: The seller creates an electronic invoice in a specific format (usually XML or UBL).

- Submission: Before sending it to the buyer, the seller must transmit the data to the government's central platform (e.g., SDI in Italy or SEFAZ in Brazil).

- Validation (The "Clearance"): The government’s system automatically checks the invoice for errors, valid tax IDs, and correct math.

- Approval: If everything looks good, the government "clears" the invoice by signing it digitally or assigning a unique authorization code.

- Delivery: Only after this approval can the invoice be sent to the buyer. In many countries, the government platform actually delivers the invoice to the buyer for you.

| Dimension | Post-audit | Clearance |

|---|---|---|

| Invoice flow | Supplier → Buyer → Payment → Tax authority | Supplier → Tax authority → Buyer → Payment |

| Government access | Months or years after the fact | Before or simultaneously with delivery |

| Invoice validity | Valid upon supplier issuance | Valid only after the government clearance stamp |

| Penalty trigger | Errors found during audit | Every failed validation is an immediate event |

| Examples | US, UK (currently) | Italy, Saudi Arabia, Mexico, Malaysia, Poland |

How does the shift to the clearance model break manual AP?

It removes the time, flexibility, and human control that manual processes depend on. What used to be a back-office, forgiving workflow becomes a real-time, system-enforced gatekeeper for every transaction.

Here’s how that specifically breaks manual AP:

-

Manual AP relies on a time buffer: invoices arrive, sit in inboxes, get reviewed, and are processed later. In the clearance model, this buffer disappears because invoices must be validated instantly by the government. As a result, manual teams cannot react fast enough, and the acceptance or rejection decision is already made before they even begin processing the invoice.

-

Manual AP often contains minor human errors, such as typos, missing tax details, or incorrect data. Before, these could be fixed later during audits. In the clearance model, even a small mistake means the invoice is rejected immediately and doesn’t count as valid. That’s why manual processes are a frequent cause of failed invoices, not just small errors.

-

Traditionally, AP teams controlled what invoices were approved and paid. In the clearance model, the tax authority validates invoices first, and only cleared invoices can proceed. As a result, manual AP loses its gatekeeping role, with approval shifting from human decision-making to government systems.

-

The clearance model requires system-to-system integration, including API connections, structured data exchange, and always-on communication with tax platforms. Manual AP, by contrast, relies on PDFs, emails, Excel spreadsheets, and manual data entry. Without automation, invoices cannot even enter the clearance process correctly.

-

The clearance model shifts compliance from an after-the-fact activity to a prerequisite for the transaction itself. In the old model, compliance was checked after transactions occurred. In the clearance model, compliance is required before the invoice even exists. As a result, manual AP cannot enforce tax rules, required formats, and validations in real time.

What is Peppol?

Peppol (Pan-European Public Procurement Online) is the global standard for secure e-invoice exchange, functioning much like the SWIFT network does for banking. By using a decentralized network of certified access points, companies can send structured XML/UBL formats directly to any government or business on the network. It reduces vendor lock-in and ensures seamless cross-border e-invoicing between countries such as Singapore and Germany.

Why do global CFOs need to care about Peppol integration?

For one simple reason: it’s quickly becoming the default infrastructure for mandatory e-invoicing worldwide. Governments are rolling out real-time reporting and structured invoice mandates, and Peppol enables companies to meet these requirements through a single, standardized connection rather than building and maintaining separate integrations for each country. That alone reduces regulatory risk and avoids constant rework as rules change.

At the same time, it dramatically cuts processing costs by minimizing manual handling, paper, and errors, while speeding up invoice cycles from days to hours through automation and direct ERP integration. Faster, validated invoices mean fewer disputes and quicker payments, improving working capital and cash flow predictability.

On top of that, Peppol enables secure, cross-border e-invoicing transactions through a trusted network with verified participants, making it easier to scale internationally without adding complexity. Bottom line: CFOs who delay adoption will face rising costs, operational friction, and regulatory exposure.

What is Peppol BIS Billing 3.0, and how is it different from a regular XML invoice?

Peppol BIS Billing 3.0 is the invoice format used on the Peppol network and is built on UBL 2.1 XML. It defines mandatory vs. optional fields, controlled tax and document codes, country-specific extensions, and Schematron validation rules. Non-compliant invoices are rejected at the access point before entering the network.

The 2025-2026 global e-invoicing map

Mandates differ across countries — some exclude smaller businesses or sectors, while others apply universally. Still, the general direction is clear: all businesses, regardless of size or industry, should prepare for e-invoicing to become the norm and not the exception.

Hover over highlighted countries to see their current mandate status and timeline:

Poland: KSeF, pre-clearance, and common pitfalls

Poland has gone live with mandatory e-invoicing, Krajowy System e-Faktur (KSeF), in waves, with the phased rollout beginning in February 2026 and extending to all VAT-registered businesses and micro-entrepreneurs by January 2027.

Timeline of KSeF rollout:

- February 2026 → Mandatory for large taxpayers with a 2024 turnover exceeding PLN 200 million, who must issue e-invoices via KSeF 2.0 in the production system.

- April 2026 → Extended to all other VAT-registered businesses, excluding micro-entrepreneurs. From this date, VAT RR invoices (for agricultural purchases from flat-rate farmers) can also be issued via KSeF.

- January 2027 → Micro-entrepreneurs must comply with both business-to-business (B2B) and business-to-government (B2G) transactions. The previous B2G "pef" platform becomes redundant.

Croatia

From 1 January 2026, all entities established in Croatia will be required to implement B2B and B2C e-invoicing. Under the Fiscalization Law, certain transactions are exempt, including public transport tickets, tolls, aircraft refuelling, utility services (electricity, gas, water, telecommunications), and in-flight sales. If the customer cannot be identified, businesses may still issue a paper invoice after this date.

Timeline:

- January 2026 → VAT-registered businesses: mandatory e-invoicing (B2B & B2G).

- January 2027 → Extended to non-VAT taxpayers and public bodies.

Greece

Greece is introducing mandatory B2B e-invoicing via the myDATA platform, in line with the EN 16931 standard. Large businesses with annual revenue above €1 million must begin issuing e-invoices from 2 February 2026, with a transition period until 31 March 2026 during which other invoicing methods can still be used in parallel.

All other taxpayers will be required to comply from 1 October 2026.

To support adoption, Greece offers strong fiscal incentives, including 100% additional depreciation on e-invoicing technology and software, as well as a full increase in deductible expenses related to the creation, transmission, and archiving of e-invoices in the first year. These incentives apply to both early adopters and companies entering the second phase, provided they meet the 2026 deadlines.

Timeline:

- 2 Feb 2026 → Large companies go live

- 31 Mar 2026 → End of transition period (for large companies)

- 1 Oct 2026 → All taxpayers in scope

Italy

A pioneer in e-invoicing, Italy has mandated B2B e-invoicing since 2019. The final exemption for micro-enterprises with turnover below €25,000 was removed on 1 January 2024, meaning the requirement now applies to all VAT-registered taxpayers. The country continues to enhance its Sistema de Intercambio (SdI) platform.

Germany

Under the Growth Opportunities Act, the obligation to receive e-invoices became mandatory from January 2025. The requirement to issue e-invoices will be phased in: from 1 January 2027 for businesses with a turnover above €800,000, and from 1 January 2028 for all businesses. Common e-invoice formats used for this purpose include ZUGFeRD, XRechnung, and Peppol, which Precoro supports as well.

Timeline:

- Jan 2025 → Mandatory to receive e-invoices

- 1 Jan 2027 → Mandatory to issue e-invoices (turnover > €800k)

- 1 Jan 2028 → Mandatory to issue e-invoices (all businesses)

Mexico

Mexico has required all taxpayers to issue digital tax invoices (CFDI 4.0) since 2011, with full pre-clearance via the SAT (tax authority) portal; no invoice is valid without real-time XML stamping and QR code validation.

B2B, B2C, and B2G apply to all economic activities; updates in 2023 tightened rules for addenda and payment complements. From 1 January 2026, stricter compliance includes mandatory "pre-validated" catalogs for products/services and enhanced e-signatures.

Timeline:

- 2011 → Mandatory e-invoicing (CFDI) for all taxpayers (real-time SAT validation)

- 2023 → Stricter CFDI 4.0 rules (addenda & payment complements)

- 1 Jan 2026 → Enhanced compliance (pre-validated catalogs + stronger e-signatures)

UAE

The United Arab Emirates is progressing toward full e-invoicing implementation by 1 July 2026. All VAT-registered businesses involved in B2B and B2G transactions will be required to comply, using a Peppol-based Decentralised Continuous Transaction Control and Exchange (DCTCE) model.

The rollout began with accreditation in early 2025, followed by pilot testing throughout 2025, ahead of full enforcement of the mandate in 2026.

Timeline:

- Early 2025 → Accreditation

- 2025 → Pilot phase

- 1 July 2026 → Mandatory e-invoicing

Singapore

In Singapore, GST-registered businesses have been able to voluntarily submit structured e-invoices to IRAS via the InvoiceNow platform since 1 May 2025. From 1 November 2025, newly incorporated companies that voluntarily register for GST are required to adopt e-invoicing.

This requirement expands further from 1 April 2026 to cover all new voluntary GST registrants. Broader mandates for existing businesses and mandatory registrants are expected, but timelines have not yet been confirmed.

Timeline:

- 1 May 2025 → Voluntary adoption

- 1 Nov 2025 → New voluntary GST registrants – newly incorporated

- 1 Apr 2026 → All new voluntary GST registrants

| Country | What changes and when? |

|---|---|

| Poland 🇵🇱 | Feb 2026: big companies must use KSeF e-Invoicing; Apr 2026: all VAT-registered businesses; fines paused until 2027. |

| France 🇫🇷 | From 1 Sep 2026: every company must receive structured e-invoices and report to tax authorities; large/medium must also issue; SMEs must issue from 1 Sep 2027. |

| Italy 🇮🇹 | Since 2019, all B2B e-invoices must go through SdI; as of 1 Jan 2024, even the smallest companies are included. |

| Germany 🇩🇪 | From 1 Jan 2025: all must receive e-invoices; from 1 Jan 2027: large companies (turnover > €800k) must issue; from 1 Jan 2028: all must issue. |

| Mexico 🇲🇽 | CFDI 4.0 mandatory since 2011 with SAT pre-clearance; 2026: stricter catalogs/audits for all taxpayers. |

| UAE 🇦🇪 | From 1 Jul 2026: all VAT-registered B2B/B2G businesses must use the new e-Invoicing system. |

| Singapore 🇸🇬 | From 1 May 2025: companies can voluntarily send e-invoices via InvoiceNow; new GST-registrants must start using it from 1 Nov 2025, with full adoption required by 1 Apr 2026; full rules for existing companies expected later. |

Top 3 most complex e-invoicing jurisdictions

Brazil e-invoicing mandate

Brazil’s Notas Fiscais Eletrônicas (NF‑e / NFC‑e) and e‑CPF / e‑CNPJ infrastructure represent one of the longest‑running and most granular e‑invoice regimes in the world.

- Layered structure: Compliance involves multiple layers, including federal, state (ICMS), and municipal (ISS) taxes, each with its own technical specifications.

- Real-time requirements: Invoices must be submitted and authorized (cleared) by the tax authorities (SEFAZ) before the goods are shipped or the service is performed.

- Constant changes: Frequent legislative changes, highly technical XML formatting requirements, and digital signature requirements make it challenging to maintain compliance.

France e-invoicing mandate

France is ranked as one of the most complex in Europe due to its upcoming, highly ambitious, and "hybrid" CTC model set for implementation between 2026 and 2027. Supported formats include Factur-X (PDF + embedded XML), CII XML, and UBL 2.1, ensuring both human-readable and structured data exchange. Precoro supports these formats, helping businesses stay compliant while simplifying the transition to France’s new digital invoicing system.

- Complex hybrid model: The framework of B2B mandate (France) combines a centralized government platform (PPF) with decentralized, certified service providers (PDPs), creating a "5-corner" model.

- Complex implementation: The mandate requires complex data exchanges, including e-reporting of invoice lifecycle status and, for some transactions, near-real-time reporting.

- Administrative hurdles: Strict adherence to local standards and the need to connect to the French platform make this a high-complexity environment for multinational corporations.

Belgium e-invoicing mandate

Belgium’s e-invoicing mandate, effective January 1, 2026, is indeed a complex "big bang" implementation that requires almost all VAT-registered businesses to shift from traditional paper or PDF invoices to structured, machine-readable XML files (Peppol BIS Billing 3.0).

- Mandatory structured data: Invoices must be in XML format and adhere to the EN 16931 standard (Peppol BIS Billing 3.0). PDFs sent by email are no longer compliant.

- Peppol network usage: Exchange must occur via the Peppol network AP, requiring companies to connect via an Access Point.

- No phased approach: Unlike other countries that phase in by company size, Belgium's mandate applies to nearly all VAT-registered businesses at once.

- 7-year archiving: All e-invoices must be stored in their structured format for seven years.

Financial penalties start at €1,500 and increase with repeated noncompliance. The planned introduction of near real-time e-reporting also means that “temporary” alternatives, such as EDI, are only a short-term option.

Why is the adoption of electronic invoicing progressing more slowly in the US?

While Europe has advanced e-invoicing through VAT-based mandates, the United States hasn’t introduced comparable requirements at either the federal or state level. Multiple factors shape the implementation of B2B e-invoicing:

- Tax structure differences: The US sales tax system is fragmented across states, which makes implementing a unified federal mandate significantly more complex.

- Voluntary adoption: E-invoicing in the US has been driven primarily by operational efficiency rather than regulatory compliance requirements.

- Industry-specific standards: Certain industries, such as healthcare (EDI 810) and retail, have independently established and adopted their own electronic invoicing standards.

- No VAT gap pressure: In the absence of a VAT system, the US does not face the same tax collection pressures that have fueled e-invoicing mandates in Europe.

Why native ERP modules fail at global e-invoicing?

Native ERP modules often fail in global e-invoicing because they’re built with an internal focus on financial stability. They can work well in a single-country setup, but once operations expand globally, complexity grows quickly. A small regulatory change in one country can trigger a domino effect, forcing updates to mappings and validations across the system. That limitation creates delays, increases costs, and adds ongoing maintenance overhead.

Here is why native ERP modules fail at global e-invoicing:

- Regulatory volatility

Tax rules change fast; native ERP can't keep up with country-specific schemas (e.g., Peppol, Brazil clearance), missing fields like tax codes, and causing rejections/fines. - Technical limitations

ERPs handle batch, not real-time clearance; synchronous tax links slow systems; diverse protocols (AS2, SFTP, REST) overwhelm them. - High costs

Ongoing adaptations for countries are expensive; customizations and multi-ERP setups (SAP, Oracle, legacy) create chaos and hidden fees. - Missing features

No built-in crypto signatures/certificates or rejection alerts; lacks proactive monitoring for global compliance.

What are the penalties for non-compliance?

Penalties for not following e-invoice mandates can be severe, including large fines, business disruption, and tax audits. They are usually charged per invoice, as a percentage of the invoice value, or up to 100% of the tax due.

- Italy – €250–€2,000 per late invoice; up to 180% of VAT for format issues.

- France – €50 per invoice; €500 per missed report (both capped at €15,000/year).

- Germany – Fines up to €5,000 per offence; VAT deduction may be denied.

- Belgium – €1,500 → €5,000 for repeated non-compliance.

- Poland – Up to 100% of VAT; additional fines for delays and missing data.

- Spain – 1–2% for errors; up to 75% for fraud; software fines up to €150,000.

Beyond fines, expect supply chain disruption — a rejected invoice means no payment, stalling deliveries, and audit nightmares, where manual errors force costly, last-minute consultant support (often $1,000 per hour for tax audit).

Benefits of mandatory e-invoices

Mandatory e-invoicing turns compliance into an advantage: it simplifies tax processes, boosts efficiency, and cuts both costs and paperwork.

Cost savings

Paper-based invoicing can quickly become expensive, with costs adding up across paper, printing, ink, packaging, and postage. Processing these invoices also carries a significant expense; in 2025, it was estimated at around $16 per invoice.

Manual processes further introduce errors, which can lead to duplicate payments, missed payments, or late-payment penalties, thereby increasing overall costs.

In comparison, e-invoicing software provides real-time visibility into invoice and payment status, helping reduce errors and improve data accuracy. It also eliminates paper-related expenses, speeds up processing, and lowers staffing and storage costs.

Tax and compliance integration

Non-compliance can lead to significant financial and reputational risk.

E-invoicing systems support compliance by integrating tax calculation and validation directly into the invoicing process. They automatically track invoice data, calculate taxes, and help prevent errors and fraud.

These systems are built to meet local regulatory requirements, making it easier for businesses to stay compliant across different markets. As a result, the risk of non-compliance is reduced, along with the likelihood of penalties or reputational damage.

Error and fraud reduction

E-invoicing systems reduce fraud risk thanks to automation and built-in controls. They:

- Transmit invoices securely via dedicated platforms.

- Track or restrict changes to maintain accountability.

- Use digital signatures to protect integrity across approval workflows.

Faster payments

E-invoicing speeds up payments and scales more efficiently than paper-based processes. Faster payment cycles improve vendor relationships and can help secure early payment discounts.

What is the benefit of a specialized AP or P2P tool for e-invoicing mandates?

Specialized AP or P2P tools shine by orchestrating the full procure-to-pay lifecycle with CTC-proof intelligence, far beyond what ERP bolt-ons offer. They ingest messy supplier invoices (PDFs, emails, portals), extract data via OCR/AI, and route them through jurisdiction-specific clearance — all while integrating bidirectionally with your ERP.

How to prepare for e-invoicing compliance and mandates

1. Review existing invoicing practices

Conduct a thorough internal assessment of your current invoicing processes to identify gaps and areas that require adjustment. Regular reviews are essential to incorporate evolving regulatory changes into your invoicing workflows and maintain ongoing AP automation compliance.

2. Choose compliant e-invoicing software

Select an e-invoicing solution that adheres to global standards and can adapt to changing regulatory requirements. A reliable provider will do both: ensure compliance and speed up operations, improve efficiency, and minimize errors.

3. Employee training

Provide targeted training for employees, particularly in finance, accounting, and IT, on e-invoicing compliance requirements. Ongoing training programs help teams stay current with regulatory updates and enable them to proactively adapt to changes.

4. Stay informed about global regulations

Continuously monitor regulatory developments across all markets in which your organization operates. Subscribing to industry updates and engaging with local regulatory authorities can significantly enhance compliance awareness and readiness.

5. Consult with compliance experts

Engage experienced compliance professionals who specialize in e-invoicing regulations. Their expertise can help navigate complex requirements, reduce AP automation compliance risks, and provide tailored solutions suited to your organization’s needs.

Automate your AP process with Precoro’s e-invoicing solution

We built e-invoicing in Precoro to cut out the manual "translation" work typically required between government tax portals and your accounting system. By handling the complex machine code entirely in the background, Precoro ensures your team stays focused on strategy, not data entry.

Frictionless invoice intake

It begins with a centralized, user-friendly inbox. When a supplier sends an e-invoice — whether in UBL, CFDI, or other regional formats — Precoro captures it instantly. Our algorithm extracts data directly from the machine code with 100% accuracy and generates a human-readable PDF, providing a familiar visual layout for effortless review.

AI-driven matching & instant drafting

The moment a file is processed, Precoro’s AI takes over. It automatically matches the invoice to the correct purchase order and generates a ready-to-submit draft in under 3 seconds. Your team simply performs a final check and clicks once to trigger the approval workflow.

High-velocity approvals

Precoro routes invoices through customizable approval chains based on department, location, or spend thresholds. Reviewers can take action from their mobile device, email, or Slack, ensuring zero bottlenecks. To keep things moving, built-in SLA tracking sends automated reminders, protecting your supplier relationships and ensuring predictable cash flow.

Seamless ERP synchronization

Once approved, Precoro pushes the invoice data to your ERP and syncs the status back once payment is issued. This two-way integration eliminates manual entry errors and keeps your records audit-ready, giving you total visibility into your financial obligations in real-time.

Actionable spend intelligence

With your entire P2P cycle centralized, you gain a "command center" view of your finances. Real-time dashboards and customizable reports track every dollar, while our AI assistant transforms raw data into strategic insights. Spot anomalies instantly, make data-backed decisions, and scale your operations without losing control.

Frequently asked questions about global e-invoicing mandates and AP automation

Invoice rules are usually set by the seller’s country (e.g., an Italian supplier must use SDI). However, the buyer’s country may still impose parallel reporting obligations; for example, ViDA compliance AP will require both parties to report intra‑EU transactions even when the other country lacks a full B2B mandate.

Some countries exempt cross‑border transactions from their domestic mandate at least initially; France, for instance, does so for its B2B e‑invoicing regime. Latin America is particularly complex: Mexico requires CFDI for exports, and Brazil requires export‑specific NF‑e documents that still pass through the domestic clearance system.

Each entity must be assessed separately, both as a seller and as a buyer.

Continuous Transaction Control (CTC) is a system in which invoice data is shared with tax authorities in real or near real time, rather than being reviewed later during audits. It matters for AP teams because every invoice becomes an immediate compliance check — errors can block payments right away, penalties apply per transaction, and tax authorities often have more complete data than the business itself. As a result, manual AP processes are no longer sufficient, and automation becomes essential.

No. Even though e-invoicing rules vary by country, you don’t need separate solutions for each mandate. Modern AP automation compliance platforms are built to support multiple regulations within a single environment.

E-billing is simply sending invoices digitally, usually as PDFs via email or a portal, so customers can view and pay them online. E-invoicing, by contrast, involves sending invoices in a structured, machine-readable format, such as XML or EDI, directly between systems, often under government rules and tax reporting requirements, especially for B2B or B2G transactions.

Don’t let compliance fall behind because of e-invoicing mandates

For finance leaders, the choice is clear: automate or get stuck. Organizations that centralize their e-invoicing strategy into a single, scalable global stack will enjoy seamless supplier relationships and clean audits. Those that delay will be forced into "retroactive remediation" — a costly, chaotic process of fixing data under the pressure of government penalties and supply chain disruptions.

Is your AP tech stack ready for 2026 mandates? Stop relying on outdated manual processes. Request a demo with Precoro and see how we can help you with global AP automation compliance and secure your financial future.

{kind=link}